Cooperativismo y Desarrollo, September-December 2025; 13(3), e894

Translated from the original in Spanish

Experience of good practices

Accounting procedures manual for real estate management companies

Manual de procedimientos contables para las empresas de gestión de inmuebles

Manual de procedimentos contábeis para empresas de administração de imóveis

Maribel Hernández Lemus1  0009-0005-5370-8541

0009-0005-5370-8541  maribelhernándezlemus@gmail.com

maribelhernándezlemus@gmail.com

Amarilys de Jesús Pozo Contrera2 0000-0001-6431-9182 amarilys@upr.edu.cu

María de Jesús Ribet Cuadot2 0000-0003-1077-4168 mariadejesus@upr.edu.cu

José García Martínez2 0000-0002-5842-2965 garcia.jose8900@gmail.com

Naidelys García Delgado2 0000-0002-2557-5121 naidelys@upr.edu.cu

1 Provincial Property Management Company of Pinar del Río. Pinar del Río, Cuba.

2 University of Pinar del Río "Hermanos Saíz Montes de Oca". Pinar del Río, Cuba.

Received: 26/03/2025

Accepted: 23/10/2025

ABSTRACT

The changes that have taken place in the Cuban economy, particularly in the retail sector,

have created a need for companies to improve their various accounting subsystems, enabling

the development of procedures that facilitate control and management decision-making. The

objective of this article is to improve accounting procedures at the Provincial Real Estate

Management Company of Pinar del Río. To diagnose the current situation, interviews were conducted

and documents were reviewed, demonstrating that the accounting procedures for leasing

premises do not comply with current regulations in the country, nor are they in line with the new

corporate purpose of this company. As a result of the research, the accounting procedures manual

was improved, consisting of five steps, the implementation of which allowed for the integration

of accounting procedures for the leasing of real estate, as well as the timely recording of

economic operations and the quality of the information provided in the financial statements of the

Provincial Property Management Company.

Keywords: manual; accounting procedures; property management.

RESUMEN

Los cambios ocurridos en la economía cubana actual

y, en particular, en el comercio minorista han incentivado la necesidad de que las empresas introduzcan en sus procesos el

perfeccionamiento de sus diferentes subsistemas contables, lo que permite el desarrollo de procedimientos

que posibiliten el control y la toma de decisiones gerenciales. El objetivo de este artículo es

perfeccionar los procedimientos contables en la Empresa Provincial de Gestión de Inmuebles de Pinar del

Río. Para el diagnóstico de la situación actual

existente, se aplicaron entrevistas y se efectuó la

revisión documental, demostrándose que los procedimientos contables para el arrendamiento de

locales no se corresponden con las normativas vigentes en el país, ni están acorde con el nuevo

objeto social de esta empresa. Como resultado de la investigación se perfeccionó el manual

de procedimientos contables, lo que quedó conformado por cinco

pasos, cuya implementación permitió la integración de los procedimientos contables para el arrendamiento de inmuebles, así como

al registro oportuno de las operaciones económicas y a la calidad de la información que se ofrece

en los estados financieros de la Empresa Provincial de Gestión de Inmuebles.

Palabras clave: manual; procedimientos contables; gestión de inmuebles.

RESUMO

As mudanças na atual economia cubana, particularmente no setor varejista, impulsionaram

a necessidade de as empresas aprimorarem seus diversos subsistemas contábeis, possibilitando

o desenvolvimento de procedimentos que facilitem o controle e a tomada de decisões gerenciais.

O objetivo deste artigo é aprimorar os procedimentos contábeis da Empresa Provincial de

Gestão Imobiliária de Pinar del Río. Para diagnosticar a situação atual, foram realizadas entrevistas

e uma revisão documental, que revelaram que os procedimentos contábeis para locação de

imóveis não estão em conformidade com as normas nacionais vigentes, nem alinhados com o novo

objetivo corporativo da empresa. Como resultado da pesquisa, o manual de procedimentos contábeis

foi aprimorado em um processo de cinco etapas. Sua implementação permitiu a integração

dos procedimentos contábeis para locação de imóveis, bem como o registro oportuno das

transações econômicas e a melhoria da qualidade das informações apresentadas nas demonstrações

financeiras da Empresa Provincial de Gestão Imobiliária.

Palavras-chave: manual; procedimentos contábeis; gestão imobiliária.

INTRODUCTION

The current international environment, characterized by constant change and

transformation, requires the improvement of accounting systems adapted to the conditions established by

the country's new economic and social model.

Cuba has not been exempt from these changes, hence the need for companies to operate

efficiently, decreeing the use of manuals of accounting standards, procedures, and policies necessary

to build a reliable and coherent financial system in line with the company's purpose, according to

its structure, number of operations, resources, and demand for products and services by

customers or users.

In addition, taking into account the provisions of the Cuban Accounting Standards

Committee, the accounting record of economic events must be made on the basis of the Cuban

Financial Reporting Standards (Ministry of Finance and Prices,

2005b).

For the proper functioning and organization of any institution, it is necessary to take into

account that adequate accounting information is essential (García Martínez et al.,

2024).

Accounting information plays a key role as it allows for the systematic and orderly

identification, recording, measurement, classification, analysis, and evaluation of all operations or

activities carried out in an organization. It is necessary for those who run the company and also for

all those who, in some way, interact with the company from outside it ("Accounting

information," 2023).

Procedures are required to obtain reliable information. According to Pozo Ceballos (2020),

a procedure is a document that clearly and unambiguously describes the consecutive steps

to initiate, develop, and conclude an activity or operation, the technical elements to be used,

the required conditions, the scope, the limitations set, and the number and characteristics of

the personnel involved.

The author himself states that accounting procedures are all those processes, steps, and

instructions used in accounting for the operations carried out by the company. With regard to analysis, it

is possible to establish accounting procedures that allow for the management of all the

general groups that make up the financial statements.

The Ministry of Finance and Prices (2005a) establishes that all entities must prepare a

document containing their accounting regulatory basis, based on the Cuban Accounting Standards, as

part of the Internal Control System.

It is therefore necessary to consider the procedures manual as an essential link in

economic activity, an inseparable part of business management with a view to achieving satisfactory

results in the economic development of entities and the country.

Accounting standards and procedures manuals contain methodological guidelines related to

the accounting recording of economic events and the issuance of financial information, as well as

the implementation of different accounting subsystems, in a single regulatory document. This

allows for quick location and uniform presentation, thus facilitating their execution, control, and updating.

For their part, Cabera Padrón et al. (2021) consider it a useful tool for staff training and

for monitoring the performance of technicians and specialists through compliance with

accounting procedures. These procedures are reliable, consistent, and in line with the requirements

of companies, according to their structure, number of operations, resources, and demand for

products and services from customers or users.

For this article, the following were taken as references: the accounting procedures manual for

an agricultural cooperative in Pinar del Río and the accounting procedures manual for companies

of the Ministry of Construction, each of which provides a detailed analysis of the

accounting subsystems, as well as the rules, policies, and information relevant to the activity carried out

by these economic actors, in addition to the regulations in force in Cuba and specifically in

their field. Although their corporate purposes differ from those of this entity, the elements that

comprise them served as a guideline for its formation.

The above authors agree that a procedure manual becomes a tool that strengthens control

and decision-making, while providing detailed, simple, orderly, systematic, and

comprehensive information on all accounting subsystems.

Hence, the improvement of accounting activities has been a priority for the country and, as

a result, various measures have been taken. However, this issue requires greater attention in

the case of the Personal and Home Technical Services companies in Pinar del Río, which belong to

the Ministry of Domestic Trade, because they faced changes in their name (Real Estate

Management Company) and, therefore, took on a new corporate purpose (renting of premises) and, as

a result, modifications were made to the branch regulations of the Ministry of Domestic Trade,

in line with the current context.

The arguments presented highlight the problem of the outdated accounting procedures

manual, which had been designed in 2015.

Based on the above, it is assumed that the scientific problem addressed in this article is:

The accounting procedures used by the Provincial Real Estate Management Company of Pinar del

Río currently have limitations in the preparation of the information they produce as part of

their management.

Therefore, its objective is to improve the accounting procedures manual at the Provincial

Real Estate Management Company of Pinar del Río.

MATERIALS AND METHODS

To diagnose the current situation of accounting procedures at the Provincial Real Estate

Management Company of Pinar del Río, different scientific research methods and techniques were used,

both theoretical and empirical. Among the theoretical methods were the historical-logical method

and the analysis-synthesis method. The historical-logical method was used to study, understand,

and determine the most significant characteristics, regularities, and trends in accounting

procedures, both nationally and internationally. The analysis-synthesis method allowed for the analysis of

the tools used for the diagnosis, as well as the characterization and analysis of this entity.

Empirical methods were used to measure the following techniques: interviews and

document review, with the purpose of determining the limitations of the accounting procedures

currently used by the Provincial Real Estate Management Company of Pinar del Río, where the

results demonstrated the scientific problem posed.

Twenty-four interviews were conducted with three managers, nine technicians, and 12

specialists from the company's economic area, as they had the greatest expertise and experience in

the activity. In addition, a document review was carried out through a bibliographic study of

the theoretical references on accounting procedures.

RESULTS AND DISCUSSION

Accounting Procedure Manuals. Analysis of the different proposed solutions

The accounting procedures manual is a set of communication tools that contain, in an orderly

and systematic manner, the information, objectives, structure, functions, and procedures of an

entity, as well as the control and classification of accounts that are transmitted to staff and serve

to regulate their actions and compliance with goals. Its purpose is to provide an up-to-date,

concise, and clear description of the activities contained in each process. Therefore, we can never

consider a manual to be complete and final, as it must evolve with the organization and be modified

to reflect current changes in the economy (Cabera Padrón et al., 2021).

It is a fundamental management tool that documents, in a written and accessible form,

the logical and chronological sequence of the processes of recording, classifying, preparing,

and presenting financial information, with the primary objective of ensuring uniformity,

reliability, timeliness, and compliance with Financial Reporting Standards and applicable legislation.

Several authors have addressed this topic and are important references for the development

of this research, including:

- The Accounting Procedures Manual for an Agricultural Cooperative in Pinar del Río,

prepared by Díaz Pando et al. (2021), provides a detailed analysis of the accounting

procedures established in a cooperative, referring to all the subsystems in accordance with

the standards, policies, and information needed to set it up. Although the social object

and purpose of cooperatives differs from our research, the elements that comprise it served

as a guideline for the development of the research.

- The Ministry of Construction's Accounting Procedures Manual for Companies is

another reference point. Its objective is to develop and apply a manual of standards and

procedures for the accounting subsystems of these companies, refined in line with current

Cuban regulations. It also outlines all the procedures necessary to first create the conditions

and then implement them, identifying all the problems that the previous manual had.

This manual is easy to understand and addresses the study of all current regulations in

the world and specifically in Cuba, establishing a methodological guide of steps to follow.

The various authors agree that a procedure manual becomes a tool that strengthens control

and decision-making, while providing detailed, simple, orderly, systematic, and

comprehensive information on all accounting subsystems.

Special features of the Accounting Procedures Manual for the Property

Management Company

The Accounting Procedures Manual for the Personal and Home Technical Services Company

of Pinar del Río, prepared by the Ministry of Domestic Trade, has served as an effective tool

for analyzing its processes, but since it changed its name to Provincial Property Management

Company, it lacks accounting procedures for its new structure, which does not allow for control and

managerial decision-making. Furthermore, it does not include financial analysis.

In diagnosing the current state of accounting procedures at the Provincial Real Estate

Management Companyof Pinar del Río, the methodology developed by Vallejos Díaz (2008) was used,

which consists of four fundamental stages:

Stage 1. Determination of information needs.

Stage 2. Definition of information sources.

Stage 3. Design of formats for information collection.

Stage 4. Data collection, analysis, and processing of information.

Each of the following stages is explained below.

Stage 1. Determination of information needs

The information analyzed made it possible to identify the patterns detected during the

investigation related to the Accounting Procedures Manual at the

Provincial Real Estate Management Company of Pinar del Río, as well as the diagnosis developed.

The information needs that were important to know were identified:

- Information related to real estate leasing in the national context, as well as new

country guidelines.

- Tools used by the Provincial Real Estate Management Company to ensure the

proper functioning of its accounting subsystems.

- Degree of updating of the procedures manual regarding laws, regulations, and

standards related to real estate leasing.

- Assessments by specialists and business decision-makers regarding the need to

improve the manual.

Stage 2. Definition of information sources

Secondary and primary sources of information were used for the characterization. The

secondary sources of information were: the company's accounting records to date, statistical

information, minutes of board meetings, chart of accounts, existing accounting procedures manual,

directives from the Ministry of Commerce, and regulations for real estate leasing.

To complement the information provided by secondary sources, primary sources were used,

applying the measurement method through individual interviews, with the aim of determining the

limitations of existing accounting procedures that affected the timely recording of economic operations

and the quality of the information provided for decision-making, where they expressed their

opinions and considerations.

Stage 3. Design of formats for information collection

The document analysis allowed for the evaluation of each of the main documents related to

the object of the research, necessary for the diagnosis.

The following tasks were carried out for the preparation and implementation of the interviews:

- Determination of the objectives of the interviews

- Preparation of the questionnaire

- Establishing criteria for selecting the sample to be applied

- Conducting the interviews

- Evaluating the information collected

Taking into account the tasks described above, the individual interview guide was designed.

Stage 4. Data collection, analysis, and processing of information

For the application of the interview, it was assessed that these met a series of criteria, which

are listed below:

- At least five years' experience in management

- Decision-making capacity on behalf of their organization

- Willingness, commitment, and honesty

- Communication and participatory leadership skills

- That they represent different levels of subordination (national, sectoral, provincial,

and municipal)

Taking these selection criteria into account, the composition of the personnel to be

interviewed was analyzed, and it was concluded that its members met the criteria. In addition,

decision-makers related to economic issues are represented in the selection.

As a result of applying the instruments and based on the analysis and synthesis of the

above documents, the following was found:

- There is no training program to inform workers about accounting procedures for

property leasing and their functionality.

- Limited knowledge among employees of the company's Accounting and Finance

Department regarding accounting procedures related to property leasing.

- The company's existing manual does not comply with current regulations in the

country, nor is it in line with the new corporate purpose of the Property Management Company.

Based on the results of the diagnosis, the Accounting Procedures Manual of the

Property Management Company was improved.

Structure of the Real Estate Management Company Accounting Procedures Manual

Accounting procedures are essential for achieving reliable information, efficient and

effective operations in the control of all types of resources available to the entity, and compliance

with established laws, regulations, and policies. The proposal is based on the criteria that should

be included in the procedures manual, as they are the most relevant to the objectives pursued in

the design of the Accounting Procedures Manual at the Provincial Real Estate Management

Company, which are based on Díaz Pando et al. (2021).

In this regard, the accounting procedures manual at the Real Estate Management Company

was structured with the following steps:

- Identification

- General index

- Introduction

- Purpose of the manual

- Accounting procedures, including: name of the procedure, purpose of the

procedure, operating rules and policies, description of the procedure, forms, and instructions

for completion

Elements to consider in each of the steps:

Identification. This refers to the first page or cover of the manual, which must include

and/or note the following information: Agency logo, Agency name, Name or acronym of the

administrative unit responsible for its preparation or updating, Title of the procedures manual, Date of

preparation or, where applicable, date of update.

Table of contents. This presents, in a summarized and orderly manner, the main items

that make up the manual. In order to standardize the presentation of these documents, it is

important to follow the order described.

Introduction. This refers to the explanation provided to the reader about the general

overview of the manual's content, its usefulness, and the aims and purposes it is intended to fulfill.

It includes information on how it will be used, who will make revisions and updates, how and

when, as well as the authorization of the agency head.

Purpose of the manual. The purpose should contain an explanation of the goal that the

procedures manual is intended to achieve.

Accounting procedures. This section lists or relates the procedures that will be described in

the manual. It is recommended that they be written in a simple, concise manner that expresses

the essence of the service. Once they are listed for each area (directorate, sub-directorate,

department), in the order in which they appear in the organizational chart of the respective

administrative unit's organization manual, each one should be analyzed, considering the inclusion of the

following points: Name of the procedure, Objective of the procedure, Operating rules and policies,

Description of the procedures, Forms and instructions for filling them out.

- Name of the procedure. At the beginning of the description, it is important to

determine the name of the procedure, which should match the name specified in the "presentation

of procedures" section and be consistent with its content. It is preferable to write it down

on a separate sheet, together with the objective and the operating rules and policies.

- Objective of the procedure. This is the goal to be achieved by developing the

procedure, which should be clear, concise, and direct.

- Operating rules and policies. These are the legal and administrative bases that

underpin the nature and purposes of an activity, established in the regulations and by

senior management, in order to provide guidance on the provision of a public service or

internal support. To this end, the areas responsible for interacting in their implementation

should be mentioned.

- Description of the procedure. This is the written narrative in chronological and

sequential order of each of the activities carried out to achieve a specific result, in response to

the fulfillment of the objective of the procedure and in accordance with its own operating

rules or policies. This definition will be supported by a methodology and a set of techniques

and tools to make it as explicit, understandable, assimilable, and, where

appropriate, transmissible as possible for the purposes of training, education, or updating of

personnel and, where appropriate, customers or users. Among the specific bases or

considerations for the description are the following:

- Use 12-point Arial font in upper and lower case when filling out the form.

- Use the formats included in the methodology that are appropriate for the needs

of each procedure, in addition to the header (Agency or Entity, Administrative

Unit, Name of Procedure, as well as the number of pages), with 5 columns containing

the following concepts: Responsible Party, Activity Number, Activity,

Format/Document, and others.

- In the "Responsible Party" row, the name of the responsible agency, body, or

position will be identified. In the case of positions, these will only be mentioned when

the nature of the activities of the corresponding agency warrants it.

- When describing the operation or activity, it should be borne in mind that

these may be perfectible, i.e., they may be improved and duplicities, unnecessary

efforts and tasks (where they exist) may be eliminated; signatures, decisions, times,

copies, formats and waiting lines may be reduced; workloads may be balanced; new

technology may be employed; and rules or policies may be reviewed, etc.

- The description shall begin with a verb conjugated in the third person singular

and present tense: initiates, prepares, presents, reviews, stores, files, consults, etc.

- When necessary, a legend can be added between each activity and/or operation

in order to give the description the required sequence, for example: when a decision

is made: "if authorized," "if correct," or when deadlines are set: "on the

established date," "subsequently," among others.

- At the end of a step, when necessary, a note or observation can be added

to complement it and also describe the destination of the originals and copies of

the forms used.

- At the end of a procedure, the phrase "End of Procedure" shall be noted.

- Forms, instructions for filling them out. The forms used in the execution of the

procedures covered by the manual should be attached at the end of the description of each

procedure, accompanied by their respective instructions for filling them out, which will contain

the corresponding indications. (Within this section, it is necessary to consider the

following: Instructions for filling out forms should only be provided for those forms that

originate within the administrative unit in question).

Below is a general overview of how the Accounting Procedures Manual was improved at

the Provincial Real Estate Management Company of Pinar del Río.

Identification (Figure 1)

Figure 1. Page header design

Source: Taken from the company

General index

- Introduction. Manual on page (1)

- Objectives and Scope. Manual on page (2)

- References. Manual on pages (2-3)

- Valuation and Disclosure Standards. Manual on pages (13-30)

- Cuban Accounting Standards. Manual on pages (30-59)

- Chart of Accounts. Manual on pages (59-166)

- Financial Statements. Manual on pages (166-196)

- Financial Analysis. Manual on pages (196-219)

- Main Accounting Procedures. Manual on pages (219-275)

Introduction

This is based on the following resolutions that authorize its preparation, establishing in its

first resolution that all state, private, and mixed companies, business groups, business unions,

state economic organizations, budgeted units, and entities in the cooperative and peasant sector

must prepare, based on the Cuban Accounting and Government Accounting Standards, a

document containing the accounting regulatory basis for each entity, as part of the Internal Control

System (Ministry of Finance and Prices, 2005a).

The name of the Provincial Technical, Personal, and Home Services Company is changed to

the Provincial Real Estate Management Company of Pinar del Río, belonging to the Trade

Business Group and subordinate to the Provincial People's Power, thus modifying the main corporate

purpose to provide real estate management services, making it necessary to update the existing

manual (Ministry of Domestic Trade, 2022).

In order to apply the principles and fulfill the functions conceived in the general organization,

the company will operate with a decentralized accounting structure, with the implication that

each Base Business Unit will record accounting events and issue a Balance Sheet, which will be

reported monthly to the Accounting and Finance Department for consolidation, which will project

an information flow through the entity's internal networks.

Objectives and Scope

The objective of the manual is to ensure greater guidance and organization in the accounting

of the Provincial Real Estate Management Company and its Base Business Units, taking

into consideration the provisions of the General Accounting Standards (Ministry of Finance and

Prices, 2005b).

Scope: The regulations apply to the entire company and its Base Business Units.

References

The procedures developed within the entity must be guided by the rules and laws

mentioned below, as the company is undergoing continuous improvement. Therefore, in preparing the

manual, each of the rules governing accounting procedures, as well as Cuban laws, will be taken

into account. This will ensure that the document is efficient and complies with the company's

internal regulations and external standards.

For the leasing of real estate, compliance with current regulations is mandatory:

- Cuban Accounting Standard No. 10 "Leases" (Ministry of Finance and Prices, 2018)

- Directives for the tendering of premises (Prime Minister, 2022)

- Apply minimum monthly rates of one hundred and twenty Cuban pesos

(120.00 pesos) per square meter (m²) of contractually leased area, except for outdoor

areas (Ministry of Finance and Prices, 2021)

- Procedure for tendering the lease of establishments and movable property of

the domestic trade system to self-employed workers (Ministry of Domestic Trade, 2021)

Valuation and Presentation Standards

The financial statements prepared by the entity must be drawn up using appropriate

uniform techniques. To this end, and based on the generally accepted principles in force in our

country, the leasing of real estate must be included, giving priority to the qualities that

accounting information must meet.

Cuban Accounting Standards

Emphasis is placed on the following standards:

- Cuban Accounting Standard No. 7 Tangible Fixed Assets (NCC No. 7)

- Cuban Accounting Standard No. 10 Leases (NCC No. 10)

Chart of Accounts

For the nomenclature of the Provincial Real Estate Management Company, its needs have

been taken into account based on the guidelines received from the Accounting Manual issued by

the Accounting Department of the Higher Organization for Business Management of Commerce

and Gastronomy, modifying it based on the guidelines contained in Resolution 494/2016 (Ministry

of Finance and Prices, 2016).

Financial Statements

Financial statements or internal accounting reports are prepared on the basis of the

characteristics and particularities of each entity and are prepared on a monthly basis. In our company, they

are mandatory.

Financial Analysis

The overall objective of financial analysis is to diagnose the company's financial situation in

terms of its liquidity, level of indebtedness, efficiency, and ability to generate profits. Specific

objectives include: evaluating the results of the activity analyzed, increasing the services provided

while improving their quality, increasing labor productivity, efficiently using productive fixed assets

and current assets, reducing the cost of services received from third parties, and achieving

planned efficiency.

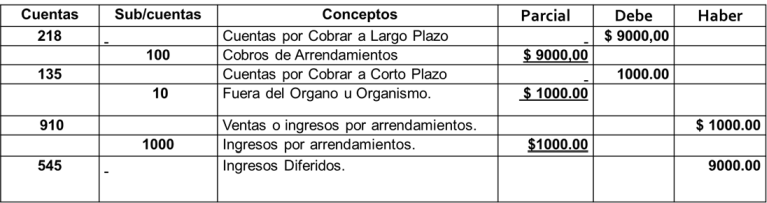

Main Accounting Procedures

An example of the main accounting procedures proposed for accounting for the initial

recognition of the lease of an asset for 10,000 pesos, with a lease or contract term of 10 years, paying

an annual fee of $1,000 pesos (Figure 2).

Figure 2. Example of the main accounting procedures proposed

Source: Own elaboration

The main contributions or benefits of its implementation have been:

- Compliance with the provisions of Resolution No. 54 of 2005 of the Ministry

of Finance and Prices.

- The accounting procedure for leases is in accordance with the provisions of

NCC No. 10.

- Opening of new account analyses in the classifier, in accordance with the

company's new corporate purpose, increasing control over material and financial resources.

- Incorporation of new headings not covered in the manual issued by the

Higher Organization for Business Management in Commerce and Gastronomy.

- Creation of a heading dedicated entirely to financial analysis, showing the

different reasons to be used by the company.

- Preparation of accounting procedures that are not widely understood by

staff in the finance department. Including those for electronic payments.

Following the implementation of the accounting procedures manual for property leasing,

the following results were obtained:

- There was a saving of 51,840.00 pesos by dispensing with the services of

the Canec (Economic Consultancy).

- Total sales from property leases increased by 30,878.5 thousand pesos during

the year.

- Economic efficiency increased, as there was no need to invest in the purchase

of raw materials and supplies, with savings in material expenses of 12,523.6

thousand pesos.

- The company's results were transformed from an annual loss of 4,156.6

thousand pesos to a profit of 14,798.9 thousand pesos.

- Contributions to the state budget increased by 30%.

- The average salary per worker increased, as did the payment of after-tax profits.

- The accounting closing period was reduced from 10 to 4 days.

The implementation of the manual enabled the integration of accounting procedures for

property leasing, as well as the timely recording of economic transactions and the quality of the

information provided in the financial statements of the Provincial Real Estate Management Company

for decision-making purposes.

REFERENCES

Cabera Padrón, N., Guerra González, M. de J., Rojas Hernández, D., & Herrera Pineda,

A. (2021). Propuesta de un manual de procedimientos contables en empresas tabacaleras. Ciencias Económicas,

2(18), e0006. https://doi.org/10.14409/rce.2021.18.e0006

Díaz Pando, J. C., Castaño de Armas, R., Falcón Corrales, D., & Rodríguez Navarro, B.

(2021). Perfeccionamiento del Manual de procedimientos contables de una Cooperativa

Agropecuaria. Cooperativismo y Desarrollo, 9(1), 314-342.

https://coodes.upr.edu.cu/index.php/coodes/article/view/313

García Martínez, J., Herrera Pineda, A., Garrido Cervera, M. M., Rizo García, I. L., &

Borges Estrada, B. L. (2024). Procedimiento para la gestión de la información contable en

empresas del sector del comercio. Cooperativismo y Desarrollo, 12(2), e680.

https://coodes.upr.edu.cu/index.php/coodes/article/view/680

Información contable. (2023). En Enciclopedia de humanidades. Equipo editorial, Etecé.

https://humanidades.com/informacion-contable

Ministerio de Comercio Interior. (2021). Resolución No. 48. Procedimiento para la licitación

del arrendamiento de establecimientos y bienes muebles del sistema de comercio interior

a trabajadores por cuenta propia. Gaceta Oficial de la República de Cuba, Edición Ordinaria

No. 31. https://www.gacetaoficial.gob.cu/es/resolucion-48-de-2021-de-ministerio-del-comercio-interior

Ministerio de Comercio Interior. (2022). Resolución No. 40. Procedimiento para la licitación

del arrendamiento de establecimientos del sistema del comercio

interior. Gaceta Oficial de la República de Cuba, Edición Extraordinaria No. 31.

https://www.gacetaoficial.gob.cu/es/resolucion-40-de-2022-de-ministerio-del-comercio-interior

Ministerio de Finanzas y Precios. (2005a). Resolución No. 54. Refiere que las entidades,

deben elaborar, a partir de la Normas Cubanas de Contabilidad y de Contabilidad Gubernamental,

un documento que contenga la base normativa contable de cada entidad, como parte del

Sistema de Control Interno. Gaceta Oficial de la República de Cuba, Edición Ordinaria No. 43.

https://www.gacetaoficial.gob.cu/es/resolucion-54-de-2005-de-ministerio-de-finanzas-y-precios

Ministerio de Finanzas y Precios. (2005b). Resolución No. 235. Dispone que el registro

contable de los hechos económicos se realice sobre la base de las Normas Cubanas de

Información Financiera. Gaceta Oficial de la República de Cuba, Edición Ordinaria No. 67.

https://www.gacetaoficial.gob.cu/es/resolucion-235-de-2005-de-ministerio-de-finanzas-y-precios

Ministerio de Finanzas y Precios. (2016). Resolución No. 494. Clasificador de Cuentas para

la actividad empresarial, unidades presupuestadas de tratamiento especial y el sector

cooperativo agropecuario y no agropecuario. Gaceta Oficial de la República de Cuba, Edición

Extraordinaria No. 39. https://www.gacetaoficial.gob.cu/es/resolucion-494-de-2016-de-ministerio-de-finanzas-y-precios

Ministerio de Finanzas y Precios. (2018). Resolución No. 942. Norma Cubana de

Contabilidad para los «Arrendatarios». Gaceta Oficial de la República de Cuba,

Edición Ordinaria No. 15. https://www.gacetaoficial.gob.cu/es/resolucion-942-de-2018-de-ministerio-de-finanzas-y-precios

Ministerio de Finanzas y Precios. (2021). Resolución No. 97. Establece la aplicación de

las tarifas mínimas mensuales por metro cuadrado de área rentada

contractualmente, por el servicio de arrendamiento de inmuebles para fines residenciales o no, y otros

servicios relacionados al inmueble que prestan las entidades estatales e inmobiliarias, las

sociedades mercantiles de capital ciento por ciento cubano y otras

autorizadas, a personas jurídicas cubanas y extranjeras, personas naturales cubanas residentes en Cuba y

extranjeras. Gaceta Oficial de la República de Cuba, Edición Extraordinaria No. 38.

https://www.gacetaoficial.gob.cu/es/resolucion-97-de-2021-de-ministerio-de-finanzas-y-precios

Pozo Ceballos, S. (2020). Selección de temas del Sistema de Control

Interno. Universidad de La Habana. Facultad de Contabilidad y Finanzas. Departamento de Contabilidad y Auditoría.

Primer Ministro. (2022). Instrucción No. 1. Directivas para la licitación de

locales. Consejo de Ministros. https://www.mincin.gob.cu/sites/mincin/files/documentos/2023-08/Instrucci%C3%B3n%201%20de%202022%20Primer%20Ministro%281%29.pdf

Vallejos Díaz, Y. A. (2008). Forma de hacer un diagnóstico en la investigación

científica. Perspectiva holística. Teoría y praxis investigativa,

3(2), 11-22. https://dialnet.unirioja.es/servlet/articulo?codigo=3700944

Conflict of interest

Authors declare that they have no conflicts of interest.

Authors' contribution

Maribel Hernández Lemus and Amarilys de Jesús Pozo Contrera participated in the literature search, study design, data collection, and manuscript preparation.

María de Jesús Ribet Cuadot, José García Martínez, and Naidelys García Delgado participated in the study design, data collection, and manuscript preparation.

All the authors reviewed the writing of the manuscript and approve the version finally submitted.

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License