Cooperativismo y Desarrollo, September-December 2023; 11(3), e688

Translated from the original in Spanish

Experience of good practices

Proposed self-monitoring guide for companies producing renewable energies

Propuesta de guía de autocontrol para las empresas que producen energías renovables

Proposta de um guia de autocontrole para empresas que produzem energia renovável

José Almeida Cordero Mederos1  0000-0002-1727-2550

0000-0002-1727-2550  jose.almeida@upr.edu.cu

jose.almeida@upr.edu.cu

Reinier González Garrido1 0000-0002-8116-5389 reinier@upr.edu.cu

Erich Márquez León2 0009-0003-4768-6177 erichmarquez64@gmail.com

Godofredo Morales Reinoso3 0000-0001-9316-3658 godofredo.morales@contraloria.gob.cu

Ibis Laritza Rizo García1 0000-0002-8915-1088 ibis.rizog@estudiantes.upr.edu.cu

1 University of Pinar del Río "Hermanos Saíz Montes de Oca". Pinar del Río, Cuba.

2 Renewable Energy Sources Company. Base Company Unit of Pinar del Río. Pinar del Río, Cuba.

3 General Comptroller's Office of the Republic in Pinar del Río. Pinar del Río, Cuba.

Received: 17/11/2023

Accepted: 12/12/2023

ABSTRACT

In current times, the production of energy through renewable sources takes on a

significant nuance, taking into account that not all economies can afford the high prices of fossil fuels

to generate electricity. This financial limitation has made Cuba define the production of clean

energy as an element of vital importance for the socioeconomic development of the country. For

the diagnosis of the current situation, several sources of information were used which, together

with scientific research methods and techniques, made it possible to know the situation of the

object of study. This article was based on the need to establish a self-control tool in the

Renewable Energy Sources Enterprise of the Base Business Unit of Pinar del Río, taking into account that

it was created through the merger of four companies belonging to different ministries. Hence,

the objective is defined as follows: To design a Self-control Guide that serves as a tool to make

the enterprise management more efficient.

Keywords: internal control; self-monitoring guide; renewable energy sources company.

RESUMEN

En los tiempos actuales la producción de energía a través de fuentes renovables cobra un

matiz significativo, teniendo en cuenta que no todas las economías pueden enfrentar los altos

precios de los combustibles fósiles para generar electricidad. Esa limitación financiera ha hecho que

Cuba defina la producción de energía limpia como un elemento de vital importancia para el

desarrollo socioeconómico del país. Para el diagnóstico de la situación actual se utilizaron varias fuentes

de información que, unidas a métodos y técnicas de investigación científica, permitieron conocer

la situación del objeto de estudio. El presente artículo se fundamentó en la

necesidad de establecer una herramienta de autocontrol en la Empresa de Fuentes Renovables de Energía de la

Unidad Empresarial de Base de Pinar del Río, teniendo en cuenta que la misma se crea mediante la

fusión de cuatro empresas pertenecientes a distintos ministerios. De ahí que se

defina como objetivo: Diseñar una Guía de Autocontrol que sirva como herramienta para hacer más eficiente la

gestión empresarial.

Palabras clave: control interno; guía de autocontrol; empresa de fuentes renovables de energía.

RESUMO

Nos tempos atuais, a produção de energia por meio de fontes renováveis assume uma

nuance significativa, levando em conta que nem todas as economias podem arcar com os altos

preços dos combustíveis fósseis para gerar eletricidade. Essa limitação financeira levou Cuba a

definir a produção de energia limpa como um elemento de vital importância para o

desenvolvimento socioeconômico do país. Para o diagnóstico da situação atual, foram utilizadas várias fontes

de informação que, juntamente com métodos e técnicas de pesquisa científica,

permitiram compreender a situação do objeto de estudo. Este artigo se baseou na necessidade

de estabelecer uma ferramenta de automonitoramento na Empresa de Fontes Renováveis

de Energia da Unidade Básica de Negócios de Pinar del Río, levando em conta que ela foi

criada por meio da fusão de quatro empresas pertencentes a diferentes ministérios. Assim, o

objetivo foi definido da seguinte forma: elaborar um guia de autocontrole que sirva como

ferramenta para tornar a gestão empresarial mais eficiente.

Palavras-chave: controle interno; guia de autocontrole; empresa de fontes renováveis

de energia.

INTRODUCTION

For Calle Álvarez et al. (2020), internal control is the fundamental element of management that must

be present in all organizations, regardless of their type and conformation. The importance lies

from the point of view of management, i.e.: it is not possible to plan, organize and manage

without control, therefore, internal control comprises an organizational plan that allows for

coordinated procedures adopted by an organization to verify the reasonableness and reliability of

financial information. In this regard, López Carvajal and Guevara Sanabria (2015) state that the

importance of having an internal control system for companies lies in the fact that through this system

the entity's processes are organized and focused on satisfying the needs at a given time, the

assets that make up the structure of the company's equity are protected and the efficiency

and effectiveness of the operations implemented are verified.

There have been several authors who, through law projects, regulations, professional

standards and guidelines, public and private reports and specialized bibliography, have discussed the

definition of internal control, but one of the most widely accepted and taken as a point of reference not

only because of the wide dissemination that has been given to it, but also because of the number

and prestige of the organizations that participated in the elaboration of the definition:

American Accounting Association, Institute of Internal Auditors, National Association of Accountants

and Financial Executives Institute was the one issued by the Committee of Sponsoring

Organizations (Coso Report), defining internal control as a process carried out by the board of

directors, management and other personnel of an entity, designed to obtain a reasonable degree of

confidence in the fulfillment of the objectives established in relation to the efficiency and effectiveness

of operations, the reliability of financial information and the respect of laws and regulations

(Coso, 2013).

Mantilla Blanco (2018) argues that it is a process performed by the board of directors,

managers and other personnel of an entity, designed to provide reasonable assurance by looking at

the fulfillment of objectives.

Other authors recognize it as a process drafted, implemented and preserved by persons in

charge of governance, by management and by other categories of personnel in order to provide

reasonable assurance regarding the fulfillment of an entity's objectives related to the credibility of

financial information, the efficiency and effectiveness of operations and compliance with adaptable

laws and regulations (Calle Alvarez et al., 2020).

Vega de la Cruz and Marrero Delgado (2021), in a study of Resolution 60 of the General Comptroller's Office of the Republic of Cuba, define the internal control system as the

process integrated to operations with a focus on continuous improvement, extended to all activities

inherent to management.

When analyzing the evolution of internal control as a management tool, it can be seen that

since the creation of the first organizations, these have had to adapt to the environment to

survive, traditional strategies are not able to respond to the requirements and demands of today's

world. It is for this reason that those that wish to survive must direct their efforts towards the

achievement of well-defined strategic objectives through management tools that allow them to diagnose

the risks of non-compliance or loss of competitive advantages.

Several authors have recognized internal control as a tool for the management of any

organization to obtain reasonable assurance for the fulfillment of its institutional objectives and to be able

to report on its management to its stakeholders

(Gamboa Poveda et al., 2016).

For López Fernández and Solís Reyes

(2018), internal control is the stage that culminates

the administrative process, in this part variations and inconsistencies are exposed based on

the objectives established by the administration, avoiding excessive economic expenses.

For the author himself, internal control is the tool that entities have to avoid any type of

economic impact resulting from non-compliance, evasion or negligence of the company's tax

obligations with the State. It is necessary to avoid incorrect calculations, payments made in an untimely

or incomplete manner in order not to produce affectations at the fiscal, labor or social level,

since employees who do not receive their correct perceptions cause excess deductions for taxes

(López Fernández & Solís Reyes,

2018).

According to the above concepts, it can be deduced that internal control is important, since

it supports management by controlling operations, verifying that resources are used efficiently.

The fact that an entity has an adequate internal control will help it maximize the use of resources

to achieve a financial and administrative management that improves the performance of the company.

For González Martínez (2019), the success of internal control lies in the juxtaposition that

exists between its components and its ease of being applied equally in all companies regardless of

their own characteristics.

Regarding the components of internal control, these are interrelated in a sequential manner,

they allow the generation of a system that acts dynamically in the face of constant changes,

both internal and in the environment where it operates. However, although companies need

the application of each component in order to control operations, no internal control model is

the same, this will depend on the scope of action of organizations, management philosophy, size

and organizational culture (Estupiñán Gaitán,

2015).

The very evolution of the definition of internal control, based on the study carried out by the

Coso report (2013), leads to affirm that the concern for improving control processes has

become widespread at the international level, supported mainly by the social concern for the quality

of financial information.

Cuba has not been far from the transformations and updates in internal control, and

although there is evidence of the methodological aspects oriented by the former State Finance

Committee, it was not until after the study conducted by the Coso commission that the need to update

the traditional approach was noted.

Authors such as Camilo Momblanc and Castro Milán (2021) state that it was not until 2003

that Cuba identified a standard that required organizations to design their internal control

system, with the Ministry of Finance and Prices issuing Resolution 297 dated September 2003, which established new criteria for the development of an internal control system adapted to the

specific conditions of each entity under the conditions of the Cuban economy.

As a result of its own evolution, the General Comptroller's Office of the Republic of

Cuba (2011) published Resolution 60 dated March 2011, which, in addition to synthesizing

the methodological aspects of the previous resolution, is more in line with the approaches

published by the Coso report. Defining it as the process integrated to the operations with a focus on

continuous improvement, extended to all activities inherent to management, carried out by the

management and the rest of the staff, implemented through an integrated system of rules and procedures

that contribute to foresee and limit internal and external risks, provides reasonable assurance to

the achievement of institutional objectives and adequate accountability.

The most significant aspect of this change is the flexibility assumed by internal control in

corporate management for each of its five components, which allows each entity to adapt it to its

own characteristics.

Cuba is a nation that for more than 60 years has been blockaded by the most powerful

and criminal empire that has ever existed in history, whose sole purpose is to try to economically

and politically suffocate Cuba for the sole crime of having made an independent nation only 90

miles from its borders. For this purpose, it has resorted to the most improbable methods such as

the creation of extraterritorial laws that harm the countries that try to establish relations and

trade with Cuba, which is why our country has been immersed in a process of adaptation and

updating of our economic model, which has the obligation to be supported by an efficient Internal

Control System, where the administration plays an important and timely role in the custody

and safeguarding of its material, financial and human resources, which allows it to fulfill its state

and social duties.

To this economic siege carried out by the empire that has affected the economic development

of the country. It is added that in the global context fossil fuels have become more expensive to

the point that for nations like ours they are practically unsustainable, so the country had to choose

to transform the energy matrix for the year 2030, where no less than 25% of this matrix will

be through the use of Renewable Energy Sources.

Although this issue was not new in the country, there was a problem: these energy

producers were diversified in different entities, for example, hydraulic generation was the responsibility

of the Hydraulic resources Company, the wind generation of the Ministry of Science, Technology

and Environment, photovoltaic generation of the Electrical Union, which, in turn, within it there

were three entities for its development, one was responsible for the search for investors, another

for the construction of the parks and the group of Renewable Energy Sources of the Electrical

Union Company for its exploitation.

Considering that these structures generated higher expenses and little control over processes,

it was decided in 2018 to begin the process of merging these entities into a single entity.

In 2019, the Hydroenergy Company merged with the Developer and Investor company of

Renewable Energy sources and thus it was begun to make practical this process. Thus, Resolution No. 43

of April 22, 2020 of the Ministry of Economy and Planning created the Renewable Energy

Sources Company.

Every organization must have an adequate system of internal controls. This allows you to

optimize processes, improve your organization's commitments and establish internal policies to help

you achieve your objectives (Grajales Gaviria et al., 2022).

Based on the above, the problem is defined as follows: Lack of a Self-Control Guide

appropriate to the characteristics of the Renewable Energy Sources Company of the Base Business Unit

of Pinar del Río, which has a negative influence on the good performance of the structure

created and the application of good practices that guarantee a more efficient management.

Specifying as objective: To design a Self-control Guide that serves as a tool to make

the management of the Renewable Energy Sources Company of the Base Business Unit of Pinar

del Río more efficient.

MATERIALS AND METHODS

During the research carried out in the Renewable Energy Sources Company of the Base

Business Unit of Pinar del Río and in the merged companies in particular, several sources of

information were used which, together with methods, techniques and analytical instruments of

scientific research, made it possible to know the situation of the object of study.

Within the theoretical methods, the historical and logical unity method was used for the

analysis of the historical evolution and current trends of internal control processes, as well as the

evolution of the evaluation of internal control in business management. The abstraction and

inductive-deductive procedure was also used, which allows, from the different positions highlighted in

the bibliography consulted, to conceptualize the elements of internal control, as well as to base

the methodology guide and establish the links between the components that make it up and

the logical sequence of its stages.

In the process of obtaining the information, all the managers, specialists and workers of

the Renewable Energy Sources Enterprise of the Base Business Unit of Pinar del Río were

involved, using the empirical method of scientific observation through the formulation of interviews

and the analysis of documents that guarantee the necessary information.

In the case of primary sources of information, a survey was conducted among those

responsible for the internal control activities of the new company, with the purpose of identifying the

main strengths and weaknesses generated by the merger of the four companies, as well as to

evaluate the participants' perception of the need for an internal control guide to address the

weaknesses mentioned.

In addition, this technique was applied to the managers of the newly created company to

determine the blind spots in terms of control caused by the newly created company, since the previous

four companies had different characteristics in their current day-to-day operations in the

accounting, logistics and operations areas.

It was also necessary to resort to secondary sources of information through documentary

analysis, including: resolutions in force on internal control, standards, legislation, guidelines,

general directives and ministerial orders issued for Renewable Energy Sources Enterprise, performance

of the self-control activity, strategic plans, control action files, audit reports, minutes of the board

of directors, company structure, internal control system established and self-control guide used

in the company, its adequacy and operability, among others.

RESULTS AND DISCUSSION

Diagnosis of the current situation of internal control in companies with renewable

energy sources

As part of this research, a diagnosis was made with the objective of recognizing the existence

of the problem and its causal relationships. Among the most relevant results obtained with

the application of the methods and techniques described above are those derived from the

interviews conducted with managers, specialists and workers and from the review of the existing

documents in the entities involved, related to the subject under investigation.

Twenty-one interviews were conducted, including one with the entity's Chief Executive Officer,

six with the main specialists in the entity's key areas and fourteen specialists and technicians

in those same areas, which yielded the following results:

- 100% (21) acknowledged being aware of the existence of Resolution No. 60/2011 of the General Comptroller's Office of the Republic and the Self-Control Guide.

- 67 % (14) recognize that Internal Control is not analyzed with the required depth, and

therefore does not constitute a working tool.

- 85 % (18) consider that the Self-Control Guide does not allow to really detect the effectiveness

of the fissures within the Internal Control mechanism, among other reasons, due to the lack

of motivation caused by its extensive and repetitive reading and analysis and the technical

language used.

- 100 % of the respondents state the lack of training and preparation on the provisions in force

and the Self-control Guide.

- 100% reported that the change of mentality has been difficult, since they come from

different companies and the methods and methodologies used in those institutions differ from the

new work and control mechanisms.

The purpose of the documentary analysis was to evaluate the operability, organization and

results of the internal control process in the merged and newly created companies. Among the

documents reviewed were, among others, the normative documents that structure internal control,

the regulations and standards in force, the Self-Control Guide and the result of its application,

the result of the juxtaposition between components, strategic objectives of the company, as well

as the legal documentation associated with the need for the creation of the Renewable

Energy Sources Company of the Base Business Unit of Pinar del Río. The development of this

analysis yielded the following results:

It was found that the Self-control Guide applied in previous years and with the old structure

of four companies consists of 279 aspects, each one of them with countless items that make

it extensive and exhausting in its management, of which only 117 are applicable to the

Renewable Energy Sources Company of the Basic Business Unit of Pinar del Río.

The study carried out revealed internal control deficiencies that were never identified with

the application of the previous guides, demonstrating the need to prepare a Self-Control Guide

based on the corporate purpose, mission and vision of the entity to make its control and

supervision more effective. Among the main deficiencies are the following:

- Deficiencies in the classification and description of Tangible Fixed Assets.

- The guide does not contemplate planning processes nor is it associated with the

company's strategic objectives; it only deals with financial accounting aspects.

- It does not consider the risks associated and inherent to the electricity generation

processes for each of the defined sources.

- Delays in economic contracting with Self-Employed or non-state forms of management.

- Lack of knowledge of standards and procedures associated with electricity generation

for each of the renewable energy sources.

- Little follow-up by the Production Councils and Boards of Directors on the

deficiencies detected during the application of the Guide.

- Although it is mandatory to review 100% of all the components of the Self-control

Guide every three months, the operational work shows that it is not being done with the

necessary depth.

- The Guide is seen as an imposition and not as a working tool.

During the work carried out, it was possible to verify, in general, progress in the

implementation process and the understanding of the actors involved on the importance of the need to

implement a Self-Control Guide adequate to the conditions of Renewable Energy Sources Company of

the Basic Business Unit of Pinar del Río, in order to guarantee a reasonable control in the

fulfillment of the strategic objectives defined by the company.

Based on the research, it has been found that the current Self-Control Guide does not meet

the needs of the new entity created, so it is necessary to update it in order to meet the new

objectives and goals. For this reason, the steps to design the guide are defined.

Design of the internal control guide appropriate to the company's specific characteristics

The proposed guide for the Renewable Energy Sources Company of the Basic Business Unit

of Pinar del Río will be structured by components, standards and procedures as established

by Resolution 60/2011 of the General Comptroller's Office of the Republic of Cuba and is

closely related to the objectives and structure for this type of enterprise. In order to establish the

new guide, the work was organized in three phases where the components of the guide are

included, which are explained below:

Phase 1. Study of the internal control aspects when the energy producing

companies operated independently

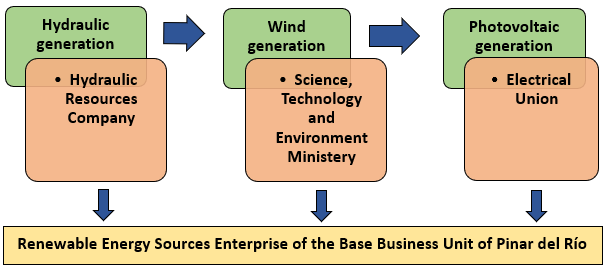

As can be seen in figure 1, the Renewable Energy Sources Company of the Basic Business Unit

of Pinar del Río was created through the integration of three companies; hence, the first step was

to study the internal control system of each of them and the positive aspects that could be

used once the new company was created and with its own characteristics.

Figure 1. Basis of integration of the Renewable Energy Sources Company of the

Basic Business Unit

Source: Own elaboration

For the study of the internal control system of each company and the positive aspects that

could be used, the internal control procedures defined for each standard according to its

components were taken into account. The analyses were based on the following results:

The company has divided its technical functions by work groups (photovoltaic investments,

hydraulic investments, repairs of these investments, maintenance), while in the newly created

company these functions will remain in a single group, which shows that the principle of separation

of functions must be transformed and with them the control activity component. This

characteristic obliges the Base Business Unit to design internal control procedures to guarantee the

separation of tasks or functions in such a way as to minimize the risks that could affect the Unit's

operational objectives.

The companies analyzed at the country level have specialists for each accounting

subsystem; however, the Basic Business Unit of Pinar del Río only has four specialists, who carry out all

the tasks related to the different accounting subsystems of the Basic Business Unit (UEB in Spanish).

The same happens in the areas of transportation, logistics and commercial, where in the case

of the UEBs and the national company, these functions are separated; in the case of Pinar del

Río, these are merged among the few specialists it has.

Phase 2. Elaboration of the self-monitoring guide according to the structure of

the components

The table below lists the standards by internal control components for which the review

techniques and procedures are developed and the efficiency of the internal control system, the

management of institutional risks, the effectiveness of operations and compliance with applicable laws

and regulations that allow the achievement of institutional objectives are evaluated. This

phase determines the reasonable success of the internal control guide as it establishes the

methodological structure for its design.

Table 1. Components and structure

Components |

Description of the Standard |

Control environment |

- Planning, annual, monthly and individual work plans

- Integrity and ethical values

- Demonstrated suitability

- Organizational structure and assignment of authority and responsibility

- Policies and practices in human resources management

|

Risk assessment |

- Risk identification and change detection

- Determination of control objectives

- Risk prevention

|

Control activity |

- Coordination between areas, separation of duties, responsibilities and authorization levels

- Timely and proper documentation and recording of transactions and events

- Restricted access to resources, assets and records

- Rotation of personnel in key tasks

- Control of information and communications technologies

- Yield and performance indicators

|

Information and communication |

- Information system, flow and communication channels

- Content, quality and responsibility

- Accountability

|

Supervision and monitoring |

- Evaluation and determination of the effectiveness of the Internal Control System

- Prevention and control committee

|

Source: General Comptroller's Office of the Republic of Cuba

(2011)

The specific aspects that make up the components and standards that comprise the guide are

as follows:

Control environment

The control environment is a set of rules, process and structure that provides the basis for

the proper conduct of the company's internal control. In this sense:

- The specificities of each standard must be

defined for the control environment component.

- Establish the standards of conduct to be followed by the personnel working in the

company and the alignment of operational and strategic values.

- In the design of the structure, the size, nature and corporate purpose of the

company must be taken into account. In the design of the control guide it should be taken

into account that the structure should contain the levels of subordination, authority

and responsibility and all should be based on the objectives defined in the first standard.

- The company's commitment to attract, develop and retain the competent personnel

that will guarantee the fulfillment of its objectives must be contemplated.

Risk evaluation

Given the laborious and extensive nature of the risk assessment in the Pinar del Río Base

Business Unit, which also works with different energy sources, it is proposed that the design of this

component contain two steps:

Step 1. Define the risk assessment structure according to its corporate purpose. The

evaluation structure must contemplate the different renewable energy sources with which the unit

works and for each of them the following elements were identified:

- Internal Environment: Provides all the information for the identification of risks.

- Setting objectives: Objectives must exist before management can identify risk

events. This ensures that management has a process in place to establish objectives to

support risk assessment.

- Event identification: Internal and external events that influence the fulfillment of

the company's objectives should be identified and classified and know whether they are

risks or represent opportunities for the company.

- Risk assessment: Risks are analyzed, considering their probability of occurrence and

the impact on the company should they occur.

- Responses to risk: In the design of the self-monitoring guide, the company must

know what management's responses to each identified risk will be (avoid, accept, reduce

or share) by developing a series of measures to align risks with their tolerance level.

Step 2. Define the roles of the other components (control activity, information and

communication, and supervision and monitoring) in the evaluation of identified risks. Risk evaluation in

companies is a multidirectional and interactive process in which all components of internal control

influence it. Therefore, in this step:

- Policies and procedures are established that are designed to ensure that risk

responses can be executed effectively.

- Relevant information and timelines should be identified in a way that allows each

person to fulfill his or her responsibilities in the risk evaluation.

- Necessary modifications are made through monitoring that allows constant evaluation

of the identified risks.

Control activity

To define the essential aspects of this component, the specificities of each standard must

be defined for the control activity component. In this component the company must:

- Select and develop control activities that contribute to minimize the identified risks

that may affect the fulfillment of business objectives.

- Take into account the development of control activities related to the types of

technology, taking into account the different energy sources that will be used.

- Include preventive and detection controls in its structure, including the design

of authorization and approval procedures, segregation of duties, performance review

and control of access to resources and evaluations of electricity generation operations, etc.

Information and communication

As part of this component, it is necessary for company managers to be able to:

- Define which information is significant to support the operation of internal control.

- Define what information is generated internally in the company, mainly those related

to the follow-up that internal control can give to the organization's objectives.

Supervision and monitoring

This component is essential for the company's internal control system, since its

implementation leads to feedback in order to improve the control process, hence:

- The company should design the evaluation system in such a way that it can have

feedback on the performance of each internal control component.

- The company evaluates and communicates the deficiencies detected in the operation

of internal control in a timely manner, in order to correct deviations with corrective actions.

Phase 3. Implementation of the Self-control Guide for the Renewable Energy

Sources Company, Base Business Unit of Pinar del Río

The implementation of the guide will be carried out through the Planning, Organization

and Control Group, promoting a better knowledge of the applicable legislation in order to know

the deviations in the different activities and work systems of the different binding work areas

and thus be able to exert a greater influence on control and prevention actions.

The Internal Control Guide, adapted to the characteristics of the UEB, will be a valuable tool

for the Internal Control System implemented, in order to achieve results with efficiency, order,

discipline and absolute compliance with the law.

UEB will have a tool for self-evaluation of the Internal Control System that will contribute

to strengthen the entity's performance, as well as the results of the control actions developed.

REFERENCES

Calle Álvarez, G. O., Narváez Zurita, C. I., & Erazo Álvarez, J. C. (2020). Sistema de

control interno como herramienta de optimización de los procesos financieros de la

empresa Austroseguridad Cía. Ltda. Dominio de las

Ciencias, 6(1), 429-465. https://dominiodelasciencias.com/ojs/index.php/es/article/view/1155

Camilo Momblanc, L., & Castro Milán, H. Y. (2021). La gestión documental y el control

interno: Un binomio indispensable. Santiago, (153), 118-129.

https://santiago.uo.edu.cu/index.php/stgo/article/view/5190

Contraloría General de la República. (2011). Normas del Sistema de Control Interno (Resolución No. 60). Gaceta Oficial de la República de Cuba, Edición Extraordinaria No.

13. https://www.gacetaoficial.gob.cu/es/resolucion-60-de-2011-de-contraloria-general-de-la-republica

Coso. (2013). Internal Control-Integrated

Framework. Committee of Sponsoring

Organizations of the Treadway Commission.

https://www.coso.org/_files/ugd/3059fc_1df7d5dd38074006bce8fdf621a942cf.pdf

Estupiñán Gaitán, R. (2015). Control interno y fraudes con base en los ciclos

transaccionales: Análisis de informe COSO I, II y

III (3.a ed.). Ecoe Ediciones.

https://www.ecoeediciones.mx/wp-content/uploads/2015/07/Control-interno-y-fraudes-3ra-Edicio%CC%81n.pdf

Gamboa Poveda, J. E., Puente Tituaña, S. P., & Vera Franco, P. Y. (2016).

Importancia del control interno en el sector público. Revista Publicando, 3(8), 487-502.

https://revistapublicando.org/revista/index.php/crv/article/view/316

González Martínez, R. (2019). Marco Integrado de Control Interno. Modelo COSO III.

Manual del Participante. Qualpro Consulting, S. C.

https://www.ofstlaxcala.gob.mx/doc/material/27.pdf

Grajales Gaviria, D. A., Giraldo Pérez, Y. E., Castellanos Polo, O. C., & Cano Bedoya, J.

(2022). Análisis del control interno en las instituciones de educación superior privadas del Valle

de Aburrá-Antioquia. Revista Virtual Universidad Católica del

Norte, (66), 161-182. https://doi.org/10.35575/rvucn.n66a7

López Carvajal, O., & Guevara Sanabria, J. A. (2015). Control organizacional: Una

mirada comparativa con el mundo. Contaduría Universidad de

Antioquia, (66), 175-190. https://doi.org/10.17533/udea.rc.26132

López Fernández, E., & Solís Reyes, E. A. (2018). La importancia del control interno para

el cumplimiento de las disposiciones fiscales en las entidades económicas. Horizontes de la Contaduría en las Ciencias

Sociales, 5(8), 157-165.

https://www.uv.mx/iic/files/2018/10/Num08-Art15-129.pdf

Mantilla Blanco, S. A. (2018). Auditoría del control

interno (4.a ed.). Ecoe Ediciones.

https://www.ecoeediciones.com/libros/auditoria-del-control-interno-4ta-edicion-ebook/

Vega de La Cruz, L., & Marrero Delgado, F. (2021). Evolución del control interno hacia

una gestión integrada al control de gestión. Estudios de la Gestión. Revista Internacional

de Administración, (10), 211-230. https://doi.org/10.32719/25506641.2021.10.10

Conflict of interest

Authors declare that they have no conflicts of interest.

Authors' contribution

Godofredo Morales Reinoso and Erich Márquez León designed the self-control guide for companies that produce renewable energies.

José Almeida Cordero Mederos and Reinier González Garrido worked on the theoretical-methodological conception of the internal control process and the self-control guide.

Ibis Laritza Rizo García carried out the data collection, analysis and interpretation.

All the authors reviewed the writing of the manuscript and approve the version finally submitted.

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License