Cooperativismo y Desarrollo, September-December 2023; 11(3), e554

Translated from the original in Spanish

Original article

Economic instruments for the environmental management: notes for Cuba

Instrumentos económicos para la gestión ambiental: apuntes para Cuba

Instrumentos econômicos para a gestão ambiental: notas para Cuba

Yusimit Betancourt Alayón1  0000-0003-2876-4670

0000-0003-2876-4670  betancourtyusimit@gmail.com

betancourtyusimit@gmail.com

Laura Sánchez Monteagudo1 0009-0008-4940-3309 laitanasanchezeco@gmail.com

Raúl Rangel Cura2 0009-0009-6260-4997 ekoraulo1979@gmail.com

Beatriz Ubieta Fernández1 0009-0003-1490-3083 beatrizubf96@gmail.com

Fátima María Dorado Corona1 0009-0005-1866-917X fatima.dorado@fec.uh.cu

1 University Havana. Havana, Cuba.

2 Institute of Tropical Geography. Havana, Cuba.

Received: 8/11/2022

Accepted: 13/10/2023

ABSTRACT

Both nationally and internationally, it has been necessary to diversify the instruments that

allow achieving the objectives of environmental policy. In all this initiative

of green the planet, there are entities which

vocation is design and implement mechanisms that modify behaviors or

grant resources that support the commitments of society and the governments for

a viable development to long term. Therefore, the objective of this work is to show, based on the analysis of the

conditions of Cuba, essential elements to design economic instruments

within their regulatory frames and capabilities for responsible environmental management. The study is located in two stages,

first capturing the national baseline in the application of economic instruments and in a

second moment the preparation of a summary of these and the implementation

advantages and limitations in the country. To do this, theoretical methods such as historical logical and documentary

analysis, as well as empirical methods such as interviews and observation are used. The role of the

legal field and structural dynamics are of great relevance to achieve the diversification of

economic instruments in the nation with greater effectiveness and acceptance.

Keywords: economic instruments; environmental management; sectors of the economy.

RESUMEN

Tanto a nivel nacional como internacional, ha sido necesario diversificar los instrumentos

que permitan alcanzar los objetivos de la política ambiental. En toda esta iniciativa

de enverdecer el planeta, existen entidades cuya

vocación es diseñar e implementar mecanismos que

modifiquen conductas u otorguen recursos que

soporten los compromisos de la sociedad y los gobiernos por

un desarrollo viable a largo plazo. Por tanto, el presente trabajo tiene como objetivo mostrar, a

partir del análisis de las condiciones de Cuba, elementos esenciales para diseñar instrumentos

económicos dentro de sus marcos

regulatorios y capacidades para la gestión ambiental responsable.

Se ubica el estudio en dos etapas, captando primero la línea base nacional en la aplicación

de instrumentos económicos y en un segundo momento la elaboración de un sumario de estos y

las ventajas y limitaciones de implementación en el país. Para ello se emplean métodos

teóricos como el histórico-lógico y el análisis documental, así como métodos empíricos tales

como entrevistas y observación. Resultan de gran relevancia el papel del ámbito legal y de

dinámicas estructurales para el logro de la diversificación de los instrumentos económicos en la nación

con mayor efectividad y aceptación.

Palabras clave: instrumentos económicos; gestión ambiental; sectores de la economía.

RESUMO

Tanto em nível nacional quanto internacional, tem sido necessário diversificar os

instrumentos que possibilitam alcançar os objetivos da política ambiental. Em toda essa iniciativa para

tornar o planeta mais verde, existem entidades cuja vocação é projetar e implementar mecanismos

que modifiquem comportamentos ou concedam recursos que apoiem os compromissos da

sociedade e dos governos para um desenvolvimento viável a longo prazo. Portanto, o objetivo deste

documento é mostrar, com base em uma análise das condições de Cuba, os elementos essenciais para

a elaboração de instrumentos econômicos dentro de seus marcos regulatórios e capacidades

de gestão ambiental responsável. O estudo está dividido em duas etapas: primeiro, a captura

da linha de base nacional na aplicação de instrumentos econômicos e segundo, a elaboração de

um resumo desses instrumentos e das vantagens e limitações de sua implementação no país.

São empregados métodos teóricos, como a análise histórico-lógica e documental, bem como

métodos empíricos, como entrevistas e observação. O papel da esfera jurídica e da dinâmica estrutural

na obtenção de uma diversificação mais eficaz e aceita dos instrumentos econômicos no país é

de grande importância.

Palavras-chave: instrumentos econômicos; gestão ambiental; setores da economia.

INTRODUCTION

Every day in an economy, decisions are made based on the use of a very diverse matrix

of Economic Instruments (IE in Spanish). They seek to influence certain growth or

development goals and, indirectly, regulate the behavior of those economic agents that deviate from

these objectives. In parallel with the desire to meet these goals, and in the absence of other

economic signals that indicate to the actors that their decisions are correct or not, a group of

environmental externalities are generated (such as pollution or overexploitation and/or loss of natural

resources), which, seen from an economic perspective, mean nothing other than a loss of capital, in

this case of a natural kind. However, this perception does not reach each economic agent in the

form of obvious signals that help correct their behavior, since, in part, external effects are not part

of the goods and services that are traded in the market, while, on the other hand, traditional

IEs are inefficient and "fail" to capture them and, therefore, induce a change in behavior. As a

result of this, a typology of instruments emerges that is classified as "economic-environmental" as

its purpose is to change the behaviors of the economic agents that generate

environmental externalities.

External environmental effects or environmental externalities not only affect an ecosystem or

a natural resource, they can be both positive and negative and depending on that, the behavior

of the agents is rewarded or corrected. However, the greatest focus of attention is occupied by

the negative external effects, which often radiate throughout society, generating, in the form of

a social cost, a loss of well-being or simply, in the form of a private cost, greater production

costs and/or lower business profitability. This type of contradiction between economic growth

and simultaneous generation of environmental externalities is not something casual, but rather

has a causal character, based on its roots in historically established patterns of production

and consumption. Faced with this type of situation, the State, in its role as a regulatory actor of

the economy, has the possibility of reversing the problems through the use of

economic-environmental instruments.

Authors such as Llanes Regueiro et al. (2012) state that, for greater effectiveness in

solving environmental externalities, it is not enough to use IE based on each environmental problem

to be resolved, but rather it is recommended that these be combined with administrative

instruments. Given the diversity of environmental externalities that are generated in the economy, not all

IEs show the same level of effectiveness, so in the literature it can be found a combination

of instruments that are effective for different types of environmental problems, or at least

for minimizing impacts and/or encouraging good behavior.

The use of IE at the service of environmental public policies has become widespread in

all countries. There is great heterogeneity in its design and application, for this reason it can

be found traditional IE adapted to environmental purposes and others that arise from a

strictly environmental perspective. The use of IE constitutes a link between policy and

environmental management.

The objective of this work is to show, based on the analysis of the

conditions of Cuba, essential elements to design IE

within their regulatory frames and capabilities for responsible

environmental management. To this end, a first section provides a general framework of the IE and the

possibilities of application in Cuba and then a section for each identified instrument. Finally, the

conclusions are presented.

MATERIALS AND METHODS

The methods used to achieve the objective of the study, taking into account a diagnostic

phase of the national context and a second space for the compilation and contribution of the

relevant elements for the identification of the different economic instruments, are conceived in a

combined way between the theoretical and the practical.

A documentary and bibliographic analysis (classical and contemporary, in Spanish and

English) is used to determine the theoretical framework of the research, systematize the concepts

and assess the trends in the use of economic instruments, synthesis of characterization for

those selected, according to the potential for application in the country, as well as their

respective implications.

A historical-logical analysis is developed in the study of the evolution of the concepts

and competencies of each of the economic instruments to be shown, by virtue of their

application conditions and other attributes of interest to the actors involved.

A systemic method is promoted that allows acting in two stages based on the decomposition

for the analysis of all the relevant elements in the application of the different economic

instruments. In addition to empirical methods such as scientific observation, based on the exchange

with experts that involve the topic at the national level, procedures are used to develop the

research such as: analysis and synthesis, abstraction and induction-deduction.

RESULTS AND DISCUSSION

Economic instruments: general aspects and perspectives for Cuba

Although in light of today there is a greater understanding of the need to use IE, there is not a

single nomenclature or taxonomy for them, using the terms "instrument", "mechanism" or

"incentive", which are also accompanied by different adjectives such as "financial", "environmental" or

"economic". Although this conceptual distinction seems trivial, in practice it generates both problems

of communication and effectiveness in its implementation.

According to Llanes Regueiro et al. (2012) the most accepted universal version of an instrument

is that of what is used to do something, while by mechanism it is understood the practical means

used in the arts. This is why there are mechanisms that try to establish how a certain instrument

or combination of them is applied to achieve some objective or goal. Consequently, they define IE

as: those that seek to achieve environmental improvement, modifying the lines of action of

people, groups, communities and corporations, through indirect regulations and incentives, preferably,

but also through negative sanctions / stimuli for not adapting to environmental regulations

(Llanes Regueiro et al., 2012). This definition makes it clear that IEs act on key economic variables such

as prices, costs or income, just to name some of the most common.

Financial instruments are conceived within the IEs. They are part of the economic incentives,

taxes, credits and specific funds, which aim to contribute to financial sustainability in the use and

conservation of natural resources and the environment, the fight against pollution and the confrontation

with climate change. Financial instruments facilitate financial solutions to environmental problems in

key sectors of the economy, based on the mobilization and redistribution of financial resources. As

they also contribute to warning the behavior of economic actors, in order to correct the main

existing environmental problems.

While financial mechanisms are a mode of operation of an economic-financial instrument that

is applied to solve, correct or mitigate a given environmental problem. Its structure will depend on

the group of actors involved, the legal regulations that regulate its operation, as well as the

characteristics of the sector and ecosystem to which it is associated.

The Economic Commission for Latin America and the Caribbean

(ECLAC, 2015) states that in terms of environmental management and policy, the most used instruments beyond the IE are:

- of Command and Control: they are regulatory in nature and establish specific standards

or limits that the different agents must comply with, for example, emission or quality standards.

- Economic: they are based on the use of economic or market incentives to generate

the desired behaviors.

- of Education and Information: they seek to educate and inform the different actors in

society about relevant aspects of the environment, such as behaviors that are

environmentally beneficial or harmful, the effects of different levels of pollution on the population and

the benefits of conservation policies, among others.

- Voluntary: are those implemented by the productive sectors, in which, through

agreements, they raise environmental protection above the levels established in the norms or standards.

Specifically, the IEs seek to achieve environmental improvement, modifying the lines of action of

the agents, in addition to generating economic resources for environmental management.

The implementation pursues adequate management of the Ecosystem Services (ES) that

ecosystems provide for the development of key sectors such as: agriculture, fishing, tourism, forestry

and conservation, under a sustainability scenario.

The use of IE in environmental management dates back to the 70s when the most

industrialized countries began their environmental policies. The use of these in solving environmental

problems comes hand in hand with the neoclassical theoretical basis of Environmental Economics.

While Ecological Economics, another of the most important disciplines within economic theory and

nature, despite doubting the convincing internalization of externalities, does not dismiss in a practical

sense how the use of these instruments helps reduce the impact of the economy about ecology. It is

then observed, from the beginning of the use of IE to the present, a growth in the variety of

instruments used, in the same way they do not have the same presence in developed countries as in

underdeveloped ones. The wide range of IE opens accordingly to the evolution and emerging needs. The areas

of application, among other subjects of environmental policy, are usually identified in: pollution

problems (waste management and recycling, changes in the quality of water, air and soil, gas and

particle emissions); resource management (water, forest, soil); biodiversity (conservation, education

and research).

The objective of the IE is that the protection and good use of the natural heritage is a

consequence of the regulation of the laws of supply and demand. They affect the costs and benefits attributable

to alternative courses of action faced by economic actors. Additionally, they offer the opportunity

to complement environmental management due to two basic advantages: 1) They introduce

greater flexibility through incentives based on prices and costs and 2) They also offer the possibility

of obtaining revenue to finance environmental management and investments through funds

specifically destined.

For these reasons, in addition to not enjoying the same level of acceptance as Administrative

or Command and Control Instruments, IEs have been gaining space. However, they are

considered regulatory instruments, perhaps the criterion is that success often depends on mixed policies

that include both types of instruments.

Once the types of instruments are defined, their origin is known for environmental policy,

therefore, the areas of application, in addition to identifying factors that condition the implementation of

the IE, are limited to: the relationship between the environmental authority and the fiscal authority,

the generation and availability of information to carry out environmental management, the

adaptation of the legal-institutional framework to enable operational environmental management, the

territorial/ regional specificity of the instruments and the political priority and institutional strength achieved

by environmental authorities.

In summary, when selecting the IE to use, one must take into account the nature of the

environmental problem to be solved, its causes, its consequences and the practical, economic, political and

ethical reality in which its design and execution.

At the national level, the policy environmental is executed through

a comprehensive management that uses a group of instruments, for a total of 14, according to the new Law of the

Natural Resources and Environment System (National Assembly of Popular Power, 2022).

Inside of the IE they conceive: financial instruments and economic incentives, taxes, credits and

specific funds, which aim to contribute to financial sustainability in the use and conservation of

natural resources and the environment, the fight against pollution and the confrontation with

climate change. Not everyone has equal

participation, neither there is a briefcase

further ambitious inside of the wide battery of Existing

IEs, however, the need for new IEs is recognized.

Based on different initiatives and projects that have been developed in recent years in Cuba,

the context is conducive to the approach and insertion into the policy of the application of EI that

link priority sectors and ecosystems, with the decision-making processes. at different scales

and allow:

- Correct and regulate the behavior patterns of actors, with a view to reversing the

latent causes of the main environmental problems identified today.

- Provide financial solutions to environmental problems in key sectors of the

economy, based on the mobilization and redistribution of financial resources that encourage

the sustainable use and conservation of the country's natural heritage.

- Promote economic, financial and environmental culture in productive and

service organizations and entities on the national and territorial scene.

Recently, at the closing of the Biodiversity Finance Initiative (BIOFIN), as

well as he Project GEF/UNDP "Incorporating

considerations environmental multiple and its economic implications,

in the management of landscapes, forests and productive sectors in Cuba" or ECOVALOR,

in execution, the need to apply several IE is identified, which are shown in table 1. They

are presented with a proposed time horizon and sectoral for implementation according to the

viability of each one, taking into account the starting conditions, inter-institutional arrangements,

among other aspects that mark the design and incorporation.

Table 1. Frame temporary and sectorial

for IE potentials

IE |

Temporary Horizon |

Key sectors of Application |

Payment for Environmental Services |

Short term |

Forest, Agriculture and Conservation |

Market of carbon |

Long term |

Forest, Agriculture and Conservation |

Tax Instruments |

Current, short and long term |

Conservation, Tourism, Industry |

Concessions |

Long term |

Tourism, Fishing |

Green Banking |

Long term |

Agriculture, Conservation |

Funds |

Current and long term |

Conservation |

Insurance environmental |

Long term |

Hydrocarbons |

Source: Prepared by the authors

The future application of these IE requires a group of adjustments in the legal and

regulatory field. Among the results and outputs committed to in the project, the

application of at least three of these IE that incorporate the economic value of SE is planned. Therefore, the strategy

to respond to these goals will be aimed at the following work objectives: 1) promote the

development of technical capabilities for the economic analysis of different environmental problems, 2)

develop standardized and legally supported methodological tools for the analysis

economic-financial analysis of different environmental problems and their solutions and 3) demonstrate the

practical viability of applying IE as a way to solve problems and generate environmental benefits.

The need to establish the critical path in the project emerges, which contributes to the

creation of technical capabilities, the design and implementation of instruments and their

incorporation into the decision-making processes. However, with a general approach, a conceptual

framework of the different IE identified is presented with a view to providing a guide for national

policy, which supports the process of selection for the sustainable management of SE by the

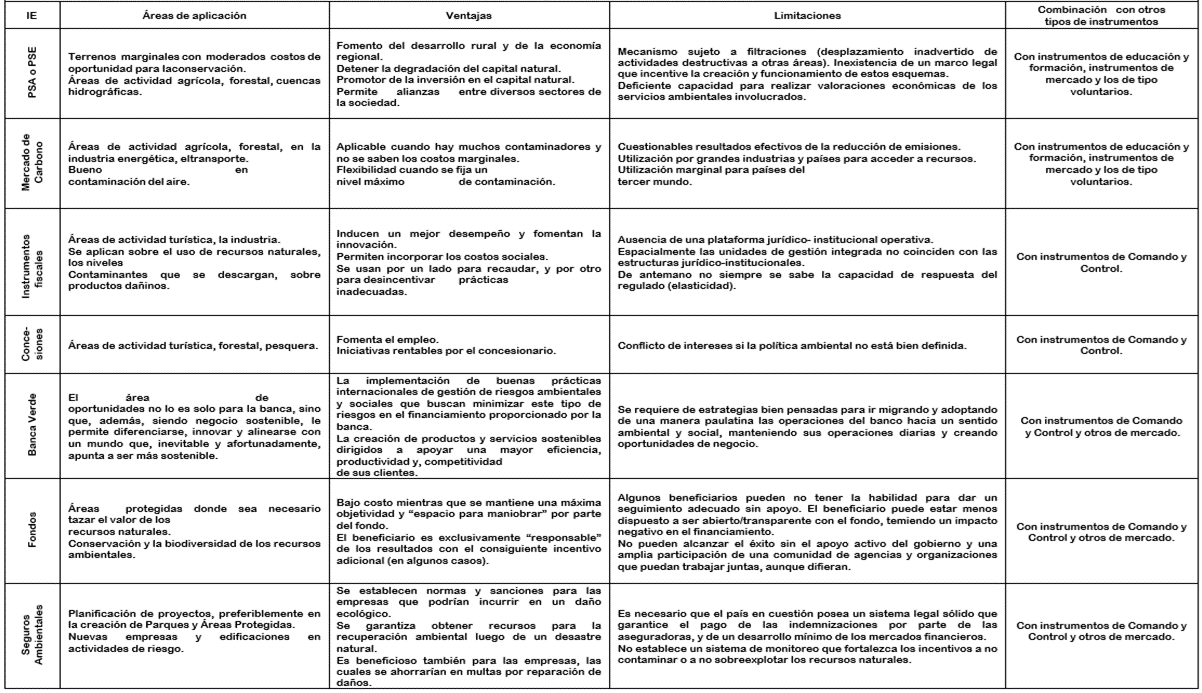

different sectors. The annex presents a summary of the applicability of the identified IE.

Conceptual frame about the IE potentials for

Cuba

Payments for Ecosystem or Environmental

Services (PSE or PSA)

This IE responds to the two challenges that raises the rural world: the conservation of nature

and the support it can provide to strategies of

development socioeconomic in the communities. The

idea central of the PSE o PSA is that the external beneficiaries of the SE pay in a

manner direct, contractual and conditional to local owners and users for

adopting practices that secure the conservation

and restoration of ecosystems.

In 2005, the Forest Research Center, in order to use it in

its research, developed a concept based on five criteria that must be met

by systems of PSE (Wunder, 2007), because the its concept

had not been materialized. The criteria for its

definition, no being exempt of critics, are stated

as follows: 1) are: a voluntary transaction, where...; 2) a well-defined ES (or a land use

that would ensure that service)...; 3) is "bought" by at least one buyer of SE...; 4)

to at least one SE provider...; 5) only if the supplier ensures the provision of the

SE traded (conditionality).

Wunder's (2007) definition is the most popular to date,

but many researchers in this area have realized that, in practice,

the most of the systems of PSE do not comply with

the five criteria proposed by him, which corresponds to the criteria of the present authors.

An essential part of this IE are the benefits that are linked to the living conditions of the

people who manage it. Thus, in recent years the concept has been expanded to include the

social benefits resulting from its implementation, seen above all in the sphere of agricultural

production: rural employment, community cohesion and other measures aimed at mitigating rural

migration. This new approach that adds specific additional investments in collateral socioeconomic

benefits is what is called Remuneration for Positive Externalities, which distances itself from

environmental problems and adds all the dimensions of sustainability.

The schemes of this instrument revolve around three groups of

SE: those related to water and soil; climate stabilization and biodiversity conservation. The benefits of ecosystem

interventions are multiple and although PES plans can focus on the improvement of one of the SE, this

will impact the others, hence the need for a comprehensive approach when implemented.

Currently, PSE are classified into three types of schemes: based on area or products, public

or private, and restricted use or productive enhancement. The most used is the first where

the contract stipulates comparable uses of the land and/or resources for a predetermined number

of land units. When they are based on products, consumers pay a `green premium', which is

a premium for production schemes certified as friendly to the environment and, especially,

to biodiversity (Pagiola & Ruthenberg, 2002). Private or public schemes refer to who the buyer

is. Private ones have a greater focus on local needs and buyers pay directly. In the case of

the public, the State is a mediator, acting in defense of the buyers of the SE, using for this

purpose the collection of taxes and requests for donations to pay the suppliers. Finally,

restricted-use PES schemes reward providers for conservation, while productive enhancement schemes seek

to restore SE in a given area.

The financing of the PSE is referred to the legislation of each country, which does not allow

its standardization. The few state financial resources require external (private) resources such

as subsidies and donations from international organizations. According to Pagdee and

Kawasaki (2021), PSE projects need the harmony generated by the application of technical expertise

and external assistance for a long time, together with financial investments and

government intervention. Until now, most PSE schemes have used cash as a payment vehicle, with

some exceptions based on in-kind payments.

Carbon market

In 1997 the Protocol of Kyoto (PK) took place, international

agreement that is derived of the United Nations Framework Convention on Climate Change. The PK wanted 37 countries and

the European Community to reduce their greenhouse gas (GHG) emissions; in this context, the

Carbon Market is born through the signing of the

nations of the world for commit to stabilizing GHGs.

It itself has as theoretical support Theorem of Coase and is defined as a trading system

through of which governments, companies or individuals can acquire or sell

GHG emissions reduction units, in order to comply with current and future obligations. What is exchanged in these

markets are certificates that represent a GHG reduction. Each certificate generally constitutes an

"X" amount of tons of CO2 equivalent (tCO2-eq.), a unit of measurement agreed upon by

the Convention Secretariat, which represents the convertibility of the various GHG gases based

on their intensity of pollution comparable to CO2. The Carbon Market has two mandatory

periods, the first of which runs from 2008 to 2012 and the second, starting with the Doha

Amendment, between 2013 and 2020. According to the KP, countries must meet their reduction

objectives, primarily through national measures, however, it also offers them an additional means to

meet their objectives through market-based mechanisms: 1) Clean Development Mechanisms, 2)

Joint Implementation and 3) Emissions Trading.

This market is usually divided into mandatory and voluntary. Voluntary Markets are

institutional systems created with the intention of reducing CO2 emissions, in States or regions that do

not have obligations within the KP. What is marketed in this case is the sale of Emission

Reductions which can be Certified or Verified, which translate into one ton of CO2. The Regulated Carbon Market is used by companies and governments that have binding legal commitments due to

the KP.

The way in which trading is carried out in the Carbon Market is like in any other market: there

is a transferable good that can be negotiated between a supplier and a demander, agreeing on

a fixed value of such good for each party. The price is complex, both in the first mandatory

period and currently, in which there is even talk of a financial bubble. Although there has been

an increase in profits, it comes from the increase in the exchange of bonds, not from an increase

in the prices of tCO2-eq, which cannot be taken as positive. Prices should be maintained at a

high enough level so that actors have sufficient incentive to change their technology to a less

polluting one. The price of tCO2-eq is essential for the Carbon Market to be an effective mechanism

to mitigate GHG emissions; that is, more and more bonds are traded in different ways, although

the price fluctuation was not what was expected. It is worth mentioning that each unit may vary

in price depending on the needs of the market and its regulation.

The steps to establish it are (ParlAmericas, 2018):

- Establish the scope of the market (geographical area, sectors, sources of emissions

and GHG that must be regulated).

- Collect robust emissions data; determine the limit level for the sectors.

- Distribute emissions rights to regulated entities while ensuring adequate oversight

to address potential leakage issues that prevent carbon emissions sources from moving

to different jurisdictions, with the intention of improving distributional impacts and

creating opportunities for governments increase income.

- Address potential price volatility and uncertainty through market stability design

features, such as a price floor, price ceiling, or emissions allowance reservations.

- Define a rigorous approach to meeting participants' obligations and for

government oversight of the system.

- Constantly collaborate with stakeholders to understand and address respective

perspectives and concerns to avoid public policy misalignment and ensure political and public support,

as well as foster collaboration between government and market actors.

- Try to link national carbon markets with international markets. This expands flexibility

in how far emissions reductions can occur, and can also improve market liquidity

and competitiveness and facilitate international cooperation.

- Enable regular reviews of market functioning, supported by rigorous and

independent evaluation, to enable continuous improvement and adaptation to changing circumstances.

Fiscal instruments

This block is made up of the most widely used IEs. The adaptation of these to the

environment identifies them as environmental taxes. Which are nothing more than the taxes, fees

and contributions that are applied for events that cause negative effects to the environment,

which causes the intervention of the State as a control entity; to do this, it collects money based

on what is established by the laws related to the event.

When designing and applying environmental taxes, it is very important to determine the

objectives for the tax, taking into account various aspects such as: collection, incentives, delimitation of

a sector, the taxpayer or, failing that, the object subject to tax. Whether the goal is the

conservation or improvement of natural resources, an environmental problem to be solved must always

be considered. This must be followed by the analysis of the contributing capacity of the

polluting agents, which must be positive. Added to this is the application of the tax principles reflected

in a legal and constitutional manner, and thus establish a structure that is made known in

a transparent manner, appealing to the environmental and tax culture. Finally, it is essential

that the simplicity of the tax structure be maintained. to avoid unnecessary costs on the part of

the tax administration and reduce the possibility of evasion and avoidance (García López, 2018).

The application of environmental taxes has advantages compared to the use of

traditional instruments that are seen in both static and dynamic efficiencies, generalizing their

collection potential; however, hypothetically the main problems lie in their distributive

impact. An environmentally related tax is one which tax base consists of a physical unit (or a

substitute thereof) of some material that has a proven and specific negative impact on the

environment. They include all taxes on energy and transportation and exclude value-added taxes

(Cepal, 2015).

Environmental taxes are characterized by mandatory payments that are

collected by he government and in which the

benefit delivered by his application is not proportional to

the payment made; for example, the collection of a tax for the emission of a pollutant into

the atmosphere either to a course of water which

collection goes destined to the general budget of

the administration of environment of the

government and no directly to reduce either treat

are emissions. An example of a tax related to the environment corresponds to the tax on fossil

fuels. Although in most national experiences this tax was developed for other purposes (for

example, collecting resources for road maintenance or other general State purposes), its

implementation generates environmental benefits through the disincentive to fuel consumption and,

therefore, it reduces associated emissions. Other examples are: taxes on energy generation, on the

circulation of motor vehicles and others. Taxes that correspond to specific charges for the use of a

natural resource should also be included, for example, a royalty for mining extraction or use of water

for specific purposes.

For their part, charges and fees are mandatory payments to the government

which Collection is more or less proportional to the services delivered, as is the

case of garbage collection rates, sewage treatment,

utilization of highways, etc.

Inside of this classification it is also included

the subsidies to the consumption and to the production which

application generates negative effects on the environment,

with independence of other socioeconomic

considerations. For example, subsidies for fossil fuels, energy

consumption, water use, irrigation and fishing, among others, should be included.

Concessions

Concession is understood as the permit, contract, agreement, license, alliance granted by

a government or administrative institution of the place to a "partner", of a special right of

temporary use over land or assets, for a determined purpose based on the pre-established conditions.

The authority that grants the Concession is the one in charge of monitoring and controlling

the agreement between both parties.

These agreements constitute a legal tool that allows natural or legal persons to take

advantage of the services provided by ecosystems, in exchange for economic remuneration (although

there are non-profit agreements), as they are considered the natural resources heritage of a

nation. Which allows diversifying recreation, tourism and other opportunities in Protected Areas

(PA).

In the case of areas with great potential for public use, it is vitally important to enter

into different models of public-private cooperation to leverage the skills and cPAital of the

business sector to manage high-quality tourism services and infrastructure to guarantee safe,

educational and unforgettable experiences to national and international visitors (Barborak, 2021).

Alliances according to the parties that make them up can be classified into three types:

public-public, public-private or private-private. Generally, on one side is the State (the grantor),

which grants non-governmental organizations, foundations, universities, private individuals,

operators, communities, companies, MSMEs (the concessionaires), through contract, the rights to use

the natural resource. At the same time, they pay for it, they are responsible for the financing

that guarantees the adequate maintenance of the service that is concessioned, under the principle

of a profitable investment, in any area that is applied. Understand, for example, the landscape

for tourism and recreational purposes, fishing, forestry, mining resources, soil and water.

The fundamental objective of the Concessions is that, through investment in

equipment, infrastructure, services and better management by third parties, an improvement in the

services offered is achieved, the satisfaction perceived by customers who are in search of contact

with nature and environmental education, and that this contributes to greater local, regional

and national development.

The experience in relation to this IE shows that, in a general sense, no institution is capable

of achieving successful PA management in a unitary manner; everything indicates that the

best functioning ones are those that normally involve several actors. At the same time, there is

a direct relationship between the size of the PA management and its managers, that is, the

larger and more complicated the management, the more actors are required.

It is important to note that the Concessions are limited to the offering of services and not

to lands (land), the latter continue to form part of the PA where the concession project is

located. Another relevant aspect is the duration of the contract, it must be sufficient for the

concessionaires to recover the investment (if it exists and taking into account its characteristics), in addition

to the opportunity to generate profits, but the grantor has the power to modify or terminate

the Concession in case of non-compliance with what was agreed by the concessionaire(s), in no

case it is recommended to reach very long-term or permanent agreements, if everything works

correctly and if it is interest of both parties the contract is renewed. The institutional framework related

to Concessions is not more or less effective, but depends on the national and local reality,

the category of management, the complexity in the management of the PA in question, among

other situational factors.

Some examples are: special events, hotels, restaurants, camping areas, transportation

services, equipment rental, tours guided by different means or local guides, sale of souvenirs and

local products, stores to purchase groceries, firewood, etc., sport fishing and hunting

(guides, companies, areas), design, construction and maintenance.

Green banking

Starting in the 90s, relationships began to be established between the banking system

and sustainability. As financial intermediaries, it became necessary to incorporate sustainability

criteria for their management; for this reason, it is possible to assume the definition of

Sustainable Banking offered by Aliciardi (2014): it is one that, by conscience and own decision of

its shareholders, directors and employees, provides products and services called "ethical" or

"green" only to clients who take into consideration the impact of their activities on the environment

and society. For a bank to be considered sustainable, it must take on the challenge of

developing, incorporating and applying corporate policies with environmental criteria based on policies

and administrative systems for evaluating credits, risks, projects, among others, so that products

and services are environmentally friendly and socially responsible.

Sustainable Banking, being a fast-moving area, many global institutions have researched

and evaluated specific initiatives related to sustainability in the sector with the aim of

accelerating and strengthening the development of good practices. Table 2 shows its main differences

with respect to Traditional Banking.

Table 2. Main differences between Traditional Banking and Sustainable Banking

Criteria |

Traditional Banking |

Sustainable Banking |

Goals |

Obtaining economic benefits |

Obtaining economic, social and environmental benefits |

Investment and financing |

Unlimited and aimed at companies that generate the greatest profits |

Restricted to socially responsible companies |

Information |

Sparse and unclear |

Transparent |

Customer preferences |

Profitability and security |

Ethical use of your money |

Customer engagement |

scarce and null |

Possibility to decide where you invest your money (environment and society) |

Credit concessions |

They grant prior credit, endorsement or guarantee |

They grant credits to viable projects, without the need for endorsements and guarantees |

Product designs |

More adapted to the needs of the bank |

More adapted to customer needs |

Decision making |

Directors and managers |

All stakeholders |

Source: Ramos López and Roiz Jique (2021)

The term has different meanings used by various stakeholders in the banking sector. Such is

the case of global actors, such as the G20 Green Finance study Group and learning networks,

the Sustainable Banking Network. These focus on green investment and environmental risk

analysis, while local initiatives are even broader and incorporate areas such as knowledge sharing

and dissemination and eco-efficiency practices. Another term related to Sustainable Banking is

Green Finance which is often considered part of Green Banking and is understood as a component of

a global initiative to protect the environment.

The Green Finance Latin America Report refers to Sustainable Banking as the group of

actions and practices carried out by a bank in the following areas:

- Green Products and Services: value proposition of a bank to meet the needs of its

clients, which incorporates environmental benefits and/or is assigned to economic activities that

are part of the green economy, understood as the transition towards low-carbon,

efficient economies resource-intensive and socially inclusive.

- Green Strategic Commitment: commitment of a bank's senior management to

Green Banking practices and environmental sustainability, also a commitment to assuming a

holistic sustainability approach within its business lines, environmental risks, eco-efficiency, etc.

- Environmental Risk Management: banking tools to manage the environmental risks

of their clients and mitigate the transfer of these risks to the bank itself.

- Internal Eco-efficiency Practices: actions and initiatives to reduce and/or mitigate

its environmental footprint and/ or optimize the use of resources through its own facilities

and networks, or through its suppliers and customers.

Sustainable Banking, Green Finance and climate finance are just some of the terms given

to practices related to climate change financing and the reallocation of financial cPAital

towards environmentally conscious practices. It is essential to homogenize and show these definitions

to deepen their development, influencing their acceleration and growth. Table 3 shows

different concepts.

Table 3. Definitions for the financial sector-environment relationship

Term |

Description |

Conservation Finance |

They are a mechanism through which a financial investment in an ecosystem is made directly or indirectly through an Intermediary, and which aims to preserve the values of the ecosystem in the long term. |

Finance for Sustainable Development |

Short-term investments for long-term sustainable development to achieve a green economy. A green economy and poverty eradication require major structural and technological changes in key sectors such as infrastructure, industry, agriculture and transport. |

Green Finance |

Mobilization of investments in environmentally sensitive areas such as agriculture, forestry, energy, mining and waste. |

Green Banking |

A green banker is not an individual, but a unit or a group or a team. Green or Sustainable Banking is not limited only to internal green activities, but extends to the facilitation of green financing. Environmental risk management guidelines are part of Green Banking to evaluate environmental risks and not to restrict investment; rather it is for Green Finance |

Ethical banking |

An organization that offers banking products that combine financial profitability with ethical aspects (social and environmental factors). Its main characteristic is that all products are ethical, although they are not focused on developing a specific sector of the economy. Its selection is based on the classification of products into positive and negative, excluding the latter. It emphasizes social inclusion, the gender struggle, the participation of interest groups and transparency. |

Source: Latin American Green Finance Report (2017)

The United Nations Environment Program - Financial Initiative (2019) and Valls Martínez et

al. (2019) when analyzing the sustainability of banking institutions, they recognize that there is

no uniform application and that the total operations still have a limited scope because

sustainable finances still do not have a priority order.

Funds

The Funds began to become widespread in the 90s. Some of

the Issues that have been subject to financing are the coverage of recurring

expenses of parks and PA, biodiversity

conservation activities and use sustainable of the

resources natural and strengthening of the

institutions local people involved in environmental conservation. From an operational

perspective, Environmental Funds can be seen in four areas of action:

1) search and catchment of resources, 2) processes

of driving of the briefcase of investment, 3) operative

mechanics of the funds and 4) execution of

activities in the field.

Environmental Funds are appropriate when existing agencies

cannot drive in an effective way the amount of

funds and the activities necessary for treating the problem, when there is a need

for new procedures or a new institution that count

with the stake and be responsible in view of the

parts interested.

To the long of the past decade, environmental funds

have been established in many countries as a way to provide long-term financing for conservation of the biodiversity

and others environmental activities. Generally, Environmental

Funds are created and managed by private

organizations and are capitalized through of subsidies of the

governments and of agencies donors, of Profits of

exchanges debt-nature and with the taxes and dues

assigned specifically for the conservation. The funds seek to provide stable financing for

the parks national and others PA, either good,

subsidize organizations private and groups

community for Projects that expand the

comprehension of the conservation of the

biodiversity using resources of manner further sustainable.

The three most common types of trust funds are: 1) Endowment funds: they spend only

the interest generated while maintaining or increasing capital; 2) Sinking funds: they liquidate

all their assets in a given period of time (for example, international projects or grants) and

3) Revolving funds: they are designed to receive regular replenishments often from various sources.

Environmental insurance

Environmental Insurance is no different from other types of conventional financial insurance

except for the fact that it is oriented towards the protection of companies or other organizations against

the risk of any ecological accident, pollution or natural disaster that causes environmental damage.

In this case, the object of the insurance is a common and freely accessible property, which functions

as a means to guarantee the cost of environmental recovery in the event that a phenomenon of

this type occurs.

The provision of Environmental Insurance guarantees the availability of savings funds to face

risks and compensation claims in the event of environmental contamination. It is, therefore, an IE

to protect both the natural environment and nearby communities from negligence on the part

of business owners in the conduct of their business and daily activities.

Unlike other types of EI for environmental protection, insurance has an ex-post effect, that is, it functions as a mechanism to finance environmental recovery once damage has occurred.

However, it could also have preventive incentives due to additional associated costs, for example, the

evaluation of the magnitude of the damages occurred and the processing of the legal process for payment

by the insurer that is usually taken to court. This is without counting the loss of corporate image

and moral and social prestige that may be generated depending on the magnitude of the event and

the reaction of the media.

Among the actors that are involved with Environmental Insurance are, first of all,

enterprises, both private and state, and whether they act as owners or operators of the area. These are the

key economic actors who can contract Environmental Insurance and who benefit from it since it

covers environmental liability risks (financial risk associated with environmental pollution) and

natural catastrophe risks (risk of significant damage in relation to the occurrence of natural disasters).

In addition, there are insurers, entities that protect companies from unforeseen losses in

exchange for insurance premiums. The greater the development of financial markets in the country in

question, the greater the diversification of insurance policy offers. Consultancies or other types of

institutions capable of carrying out environmental risk and damage assessments are also important actors,

both in estimating the insurance premiums to be paid and in the amount of compensation once

the disaster occurs.

Legal institutions also play a fundamental role since they regulate Environmental Insurance

and define the guidelines from a contractual point of view. Conflict resolution in courts to obtain

payment from insurers in the event of ecological accidents is common. Therefore, a solid legal system

is needed for this IE to be viable. Environmental advocacy groups, international aid agencies,

local governments, nearby communities and the media are also key actors who can influence the

terms and conditions around Environmental Insurance.

In short, not all risks are insurable, while many are insurable only under certain parameters.

These basic conditions are: that the risks must be distributed, that they must be reasonably well

defined, be limited in time and be measurable, they must also be calculable from historical data or

available information, there must be mechanisms to overcome moral hazard and adverse selection, in

addition to the fact that any contract must be enforceable

(Hidalgo Chávez & Rendón Schneir,

2021). However, it should not try to overvalue them; issues such as biodiversity and climate change

cannot be insured.

There is a legal-institutional framework that advocates and expands the use of IE in the

country. Environmental policy places them on different deadlines given the complexity and need

for changes that these require. The IE range covers an important sectorial range with a view

to enabling each individual economic development policy to catalyze synergies between them

and where the environmental dimension is the transversal one that guides the development of

the country towards sustainability. The feasibility of applying each one rests on different

elements that impose challenges on the design of environmental policy and its link with legal aspects

and economic policies. The success of design and implementation depends on the gearing.

REFERENCES

Aliciardi, M. B. (2014). Bancos y sostenibilidad ambiental: ¿Bancos

sostenibles? Federación Latinoamericana de Bancos / Comité Latinoamericano de Derecho Financiero.

https://dokumen.tips/documents/maria-belen-aliciardi-bancos-y-sostenibilidad-ambiental.html?page=1

Asamblea Nacional del Poder Popular. (2022).

Ley del Sistema de los Recursos Naturales y el Medio

Ambiente (Ley 150). Gaceta Oficial de la República de Cuba, Edición

Ordinaria No. 87. https://www.gacetaoficial.gob.cu/es/ley-150-de-2022-de-asamblea-nacional-del-poder-popular

Barborak, J. R. (2021). 30 % para 2030: América Latina y la nueva meta global para

sus sistemas de áreas protegidas. Revista de Ciencias

Ambientales, 55(2), 368-378. https://doi.org/10.15359/rca.55-2.19

ECLAC. (2015). Guía metodológica: Instrumentos económicos para la gestión

ambiental. Comisión Económica para América Latina y el Caribe.

https://www.cepal.org/es/publicaciones/37676-guia-metodologica-instrumentos-economicos-la-gestion-ambiental

García López, T. (2018). Instrumentos económicos para la protección ambiental en el

derecho ambiental mexicano. Sociedad y

Ambiente, (17), 247-266.

https://revistas.ecosur.mx/sociedadyambiente/index.php/sya/article/view/1836

Hidalgo Chávez, A. A., & Rendón Schneir, E. (2021). ¿Seguro ambiental obligatorio en el

Perú? Sociedad y Ambiente, (24), 1-31. https://doi.org/10.31840/sya.vi24.2328

Informe Finanzas Verdes Latinoamérica. (2017). ¿Qué está haciendo el sector bancario

de América Latina para mitigar el cambio

climático? International Finance

Corporation. https://www.ifc.org/wps/wcm/connect/950f6389-72aa-482c-b5c6-e7dc7511cdc2/Green+Finance+Report_Informe+Finanzas+Verdes_2019.pdf?MOD=AJPERES&CVID=mGxkh40

Llanes Regueiro, J., Betancourt, Y., Ferro Azcona, H., & Rangel Cura, R. A. (2012). Introducción a la Economía

Ambiental. Universidad de La Habana.

https://isbn.cloud/9789597211204/introduccion-a-la-economia-ambiental/

Pagdee, A., & Kawasaki, J. (2021). The importance of community perceptions and

capacity building in payment for ecosystems services: A case study at Phu Kao,

Thailand. Ecosystem Services, 47, 101224. https://doi.org/10.1016/j.ecoser.2020.101224

Pagiola, S., & Ruthenberg, I.-M. (2002). Selling biodiversity in a coffee cup:

Shade-grown coffee and conservation in Mesoamerica. En S. Pagiola, J. Bishop, & N.

Landel-Mills (Eds.), Selling forest environmental services. Market-based mechanisms

for conservation and development (pp. 103-126)). Routledge.

https://www.routledge.com/Selling-Forest-Environmental-Services-Market-Based-Mechanisms-for-Conservation/Pagiola-Bishop-Landel-Mills/p/book/9781853838880#

ParlAmericas. (2018). Manual sobre la fijación del precio del

carbono. ParlAmericas. http://parlamericas.org/uploads/documents/ParlAmericas-CarbonPricing_ES.pdf

Programa de las Naciones Unidas para el Medio Ambiente. (2019).

Principios de banca responsable. Guía de

implementación. International Environment House.

https://www.unepfi.org/wordpress/wp-content/uploads/2022/07/PRB-Guidance-Document-Spanish-Principios-Para-La-Banca-Responsable-Documento-Guia.pdf

Ramos López, E., & Roiz Jique, J. (2021). Banca sostenible: Apuntes para Cuba. COFIN Habana, 15(2). https://revistas.uh.cu/cofinhab/article/view/625

Valls Martínez, M. del C., Cruz Rambaud, S., & Parra Oller, I. M. (2019). Banca ética en

Europa. Comparativa con la banca tradicional. En Diverstiy and talent: Synergistic effects in

management (pp. 352-376). European Academic Publisher.

https://www.researchgate.net/publication/334560813_Banca_etica_en_Europa_Comparativa_con_la_banca_tradicional

Wunder, S. (2007). The efficiency of payments for environmental services in

tropical conservation. Conservation Biology,

21(1), 48-58.

https://doi.org/10.1111/j.1523-1739.2006.00559.x

Conflict of interest

Authors declare that they have no conflicts of interest.

Authors' contribution

Yusimit Betancourt Alayón: Originated the idea of the article, compiles information, analyzes, studies and reflects on the EI for environmental management, debates on the advantages and disadvantages of these for the case of Cuba. Particularizes on Fiscal Instruments and Funds.

Laura Sánchez Monteagudo: Gathers information and conducts a study on EI for environmental management (with particular emphasis on Payment for Ecosystem Services, Carbon Market and Green Banking), the conditions Cuba has to develop them within its regulatory frameworks and capacities for responsible environmental management.

Raúl Rangel Cura: Gathers information and conducts a study on EI for environmental management, methodological and conceptual aspects, the conditions Cuba has to develop them within its regulatory frameworks and capacities for responsible environmental management.

Beatriz Ubieta Fernández: Gathers information and conducts a study on EI for environmental management (particularly on Environmental Insurance), the conditions Cuba has to develop them within its regulatory frameworks and capacities for responsible environmental management.

Fátima María Dorado Corona: Gathers information and conducts a study on EIs for environmental management (particularly on Concessions), the conditions Cuba has to develop them within its regulatory frameworks and capacities for responsible environmental management.

ANNEXES

Figure 1. Synthesis of applicability of the IE identified in national environmental management

Source: Prepared by the authors

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License