Cooperativismo y Desarrollo, May-August 2023; 11(2), e528

Translated from the original in Spanish

Original article

Conceptualization of economic-financial instruments for environmental management in Cuba

Conceptualización de instrumentos económicos financieros para la gestión ambiental en Cuba

Conceitualização de instrumentos econômico-financeiros para gestão ambiental em Cuba

Yenisleidys Monzón Aldama1  0000-0002-1946-197X

0000-0002-1946-197X  yenisleidys.monzon@umcc.cu

yenisleidys.monzon@umcc.cu

Sheila Pérez Díaz1 0000-0003-3875-4206 shpd1999@gmail.com

Mercedes Marrero Marrero1 0000-0003-0804-2048 mercedes.marrero@gmail.com

Maritza Petersson Roldán1 0000-0002-0453-3571 maritza.petersson@gmail.com

María Leandra Pascua Migueles1 0000-0003-0762-4302 marialeandrapascua@gmail.com

1 University of Matanzas "Camilo Cienfuegos". Matanzas, Cuba.

Received: 14/07/2022

Accepted: 6/06/2023

ABSTRACT

There are numerous factors that today have a direct impact on the environment, affecting

and deteriorating it more and more. The economic and productive activities carried out by man

that involve highly polluting industrial processes and procedures are fundamental agents that have

an impact on the visible deterioration of the environment. Precisely from this arises the need for

the industrial and business sector, as well as the private sector, to be aware of the damage caused

by the emissions derived from their actions. The State, in turn, is responsible for using

economic and financial instruments to encourage these agents to use environmental management in

each process in a responsible manner. The proposed objective is to

define the concept of economic and financial instrument for environmental management in Cuba based on the theoretical

foundations studied. The inequality of definitions given by the preceding authors

is synthesized through the analysis of the recommended bibliography on the subject and the recapitulation of the

aspects consulted, induction and deduction, as well as the historical-logical method

provides a concept of financial economic instruments for environmental management, which becomes the

fundamental axis of the research entitled: "Conceptualization of financial economic instruments for

environmental management in Cuba", in which the theoretical elements that sustain the financial

economic instruments in the environmental context are defined, which encourage the use of the same

in Cuba to contribute to the reduction of environmental pollution.

Keywords: financial economic instruments; environmental management; environment.

RESUMEN

Son numerosos los factores que hoy inciden de manera directa en el medioambiente,

afectándolo y deteriorándolo cada vez más. Las actividades económicas y productivas realizadas por el

hombre que involucra procesos y procedimientos industriales altamente contaminantes son

agentes fundamentales que inciden en el visible deterioro del ambiente. Precisamente de ahí surge

la necesidad de que se tome conciencia por parte del sector industrial, empresarial, como por

el privado, del daño que provocan las emisiones derivadas de su actuar. Es el Estado, a su vez,

el encargado de utilizar instrumentos económicos y financieros que incentiven a estos agentes

a hacer uso de la gestión medioambiental en cada proceso de manera responsable. El

objetivo propuesto es definir el concepto de instrumento económico financiero para la gestión

ambiental en Cuba a partir de los fundamentos teóricos estudiados.

La desigualdad de definiciones dadas por los autores

precedentes se sintetiza mediante el análisis de la bibliografía

recomendada sobre el tema y la recapitulación de los aspectos consultados, la inducción y deducción, así

como el método histórico-lógico

brinda un concepto de instrumentos económicos financieros para

la gestión ambiental, el cual se convierte en el eje fundamental de la investigación

titulada: "Conceptualización de instrumentos económicos financieros para la gestión ambiental en

Cuba", en la cual se definen los elementos teóricos que sustentan los instrumentos económicos

financieros en el contexto ambiental, que incentivan la utilización de los mismos en Cuba para contribuir a

la reducción de la contaminación del medioambiente.

Palabras clave: instrumentos económicos financieros; gestión ambiental; medioambiente.

RESUMO

Atualmente, existem inúmeros fatores que têm impacto direto sobre o meio ambiente,

afetando-o e deteriorando-o cada vez mais. As atividades econômicas e produtivas realizadas pelo

homem, que envolvem processos e procedimentos industriais altamente poluentes, são

agentes fundamentais que impactam na visível deterioração do meio ambiente. Justamente por

isso, surge a necessidade de que o setor industrial e empresarial, bem como o setor privado,

estejam cientes dos danos causados pelas emissões resultantes de suas ações. O Estado, por sua vez,

é responsável por utilizar instrumentos econômicos e financeiros para incentivar esses agentes

a fazer uso responsável da gestão ambiental em cada processo. O objetivo proposto é definir

o conceito de instrumentos econômicos e financeiros para a gestão ambiental em Cuba, com

base nos fundamentos teóricos estudados. A desigualdade de definições dadas pelos autores

anteriores é sintetizada por meio da análise da bibliografia recomendada sobre o assunto e a

recapitulação dos aspectos consultados, a indução e a dedução, bem como o método histórico-lógico,

fornecem um conceito de instrumentos econômico-financeiros para a gestão ambiental, que se torna o

eixo fundamental da pesquisa intitulada: "Conceitualização de instrumentos econômicos

financeiros para a gestão ambiental em Cuba", na qual se definem os elementos teóricos que sustentam

os instrumentos econômicos financeiros no contexto ambiental, os quais incentivam o uso dos

mesmos em Cuba para contribuir com a redução da poluição ambiental.

Palavras-chave: instrumentos econômico-financeiros; gestão ambiental; meio ambiente.

INTRODUCTION

The environment is seen as a set of basic conditions that surround human beings in their

integrality and force them to assume a coherent and responsible attitude, capable of resulting in

concrete actions of protection that strengthen the balance that must exist between the elements of

nature that make possible the prolongation of life on Earth, where the subjective right to enjoy a

healthy environment needs a type of culture immersed in this problematic to understand the scope of

its role (Koellner et al., 2019).

It is therefore imperative that renewable natural resources be used below their annual

renewal rate, respect the assimilation margins of the environmental vectors (air, water and soil) and,

in addition, that their use be environmentally integrated with economic development. The

problem of environmental deterioration and transboundary pollution has reached such a crucial point

that there is no room for lamentation or mutual blame. The damage has been done and the only

thing left to do is to seek strategies and mechanisms to mitigate its impact, even beyond

economic limitations. The dilemma that remains is: to be or not to be

(Vargas et al., 2019).

Latin America and the Caribbean have natural capital (land, forests) and non-renewable

resources (oil, gas and minerals) that contribute 17% to the growth of its wealth, making it the region

with the second highest contribution of natural capital to its wealth, after the Midwest and

North Africa region. This natural capital is not only important for the region's economic growth,

but represents considerable global capital when taking into account that, although the region

represents only 16% of the planet's landmass, it provides and safeguards important natural resources

and ecosystem services (Durango et al., 2019).

Among the international organizations that promote the adoption and implementation of

specific documents aimed at strengthening the environmental protection approach, the United

Nations Environment Program stands out, with an impact on marine protected areas in an

integrated coastal and marine management approach, as well as the United Nations Development

Program, which provides countries with tools for capacity building and enhances knowledge in

environmental management with an integrated approach to achieve sustainable development. The United

Nations Educational, Scientific and Cultural Organization through the Intergovernmental

Oceanographic Commission is a key promoter of research that contributes to the management of the seas

and coasts (Vázquez Sosa et al., 2020).

Society must learn to live in harmony with ecosystems, since in the modern world all

exploitation of the products and services they provide is expressed in impacts on them. It is

extremely necessary to incorporate the importance of the care and conservation of coastal ecosystems

into the conscience of citizens, as well as all institutions that can provide solutions through which

this problem does not become a danger to human survival, as well as other species that are at risk.

Today, the environmental issue is identified with the most important concerns of humanity,

where it occupies a central place both in the theoretical debate and in the decision-making process.

In Fidel Castro's socioeconomic thinking in the 1990s, two key ideas stand out: the first refers

to the link between the environment and development, and the second to the need to observe

and be consistent with the laws of nature, that is, to make rational use of natural resources.

Environmental degradation is the set of damages suffered by the environment in reference to

the natural surroundings and each of its components, and is directly related to the way a

country develops its economic activities and the procedures it uses to exploit its natural resources.

The accelerated and increasing deterioration of the environment is today possibly the most

serious long-term danger facing the entire human species as a whole.

Economic science also faces the search for solutions, to the environmental problematic based

on multidisciplinarity, with the purpose of protecting and conserving the services offered by

ecosystems (Molina & Rodriguez and Silva,

2019).

Environmental economics is a subdiscipline of knowledge that analyzes the adverse

environmental effects of the processes of production and consumption of goods and services from an

economic perspective and proposes economic instruments for the prevention and treatment of

environmental impacts. It draws on macroeconomics and microeconomics to combat the causes and

consequences of the degradation of the natural environment by human activity

(Canova et al., 2019; Pérez Calderón,

2010).

On the other hand, ecological economics is not a pure branch of the economic sciences, but

a multidisciplinary field of study. The basic problem it studies is the sustainability of the

interactions between the economic system and the natural macrosystem. Such sustainability

understood within environmental limits (Canova et al.,

2019).

To address the root causes of the environmental problem, it is necessary to adopt measures

in the decision-making process that integrate the costs and benefits of altering the

environment. This can be achieved by different means, such as establishing regulations, convincing and

involving all stakeholders (entities, government, Ministry of Science, Technology and Environment

(Citma) and the population in general), or through economic instruments of environmental policy

that can contribute to minimize or repair the effects caused by man.

In Cuba, Citma governs the National Biodiversity Strategy, which establishes, among its

guiding principles, the development and application of environmental economics with the objective

of applying economic instruments and social incentives for decision making

(Monzón Aldama et al., 2022).

Economic instruments constitute a category within Environmental Regulatory Instruments,

which affect the costs and benefits attributable to various courses of action faced by different

economic agents, affecting, for example, the profitability of alternative processes or technologies or

the relative price of a product and, consequently, the decisions of producers and consumers.

In other words, the systems of economic instruments for the environment are a state

mechanism of intervention in the economy, with the sole purpose of influencing, on the one hand, the

price structure, the levels of profitability or affordability, as the case may be and, therefore,

the competitiveness of enterprises and, on the other hand, producers and consumers, aiming

to modify their negative behavior towards the environment, as well as demand

(Biointropic, 2022).

From the microeconomic point of view, the application of the instruments should lead polluters

to correct prices to include the social costs generated. It is also expected that consumers will

make adjustments and demand fewer polluting products and modify their consumption patterns

(Damania et al., 2020).

Taxation of polluting goods or services can be expected to generate price increases

and, consequently, inflation. That is, when polluters introduce true social costs into private costs,

this increase is usually passed on to consumers. It is also possible that they lead to a loss

of competitiveness for high-cost sectors because they include social costs and pass them on

to consumers. But it is also possible that environmental fiscal instruments may

encourage technological change and innovation, orienting production towards more efficient processes

in the use of raw materials and waste disposal.

Hence, the option of employing economic instruments that contribute to minimizing

environmental impacts, confronting climate change and, in particular, protecting and conserving

ecosystems, has played an important role, since it provides the possibility of creating financial

economic mechanisms to support environmental management models in vulnerable

environments (Vihervaara et al., 2019).

In this sense, it is vital to understand the concept of economic financial instrument as a way

to encourage its use in optimal conditions for environmental protection and conservation and

the preparation of scenarios for its application. Therefore, the objective is: To define the concept

of economic and financial instrument for environmental management in Cuba, based on the

theoretical foundations studied.

MATERIALS AND METHODS

In order to obtain results in this research, dissimilar methods of the theoretical and

empirical level were applied, starting from a dialectical-materialist approach, which provided the

analysis of the recommended bibliography on the subject and the recapitulation of the aspects

consulted, determining the main contradictions and links between the elements of the object of

study, leading the research to the search for new regularities and the unification of concepts.

Induction and deduction are two fundamental theoretical methods for the research to achieve

the justification of the importance of conceptualizing financial economic instruments in

environmental management.

Among the methods of the theoretical level, the historical-logical method was applied in

the research, which made possible the analysis of the theoretical references associated with

the economic-financial instruments for environmental management in Cuba and in the world,

which allowed revealing their essence, definitions, categories, classification for management, as well

as their use in Cuba and their current importance at the national and international level.

As for the empirical methods used in the research, the bibliographic review stands out,

where documents, reports, books that explicitly cover the topics addressed by the research were

reviewed, through which the definition of financial economic instruments, their current influence and

the need for the use of financial economic instruments in environmental management could

be confirmed.

RESULTS AND DISCUSSION

Economic activities have consequences that affect not only those who decide to carry them

out, but also third parties. These consequences are called externalities. These refer to the behavior

of certain economic agents that cause costs or benefits (negative or positive externalities) to

third parties in compensation for this. In these cases, the goods and services markets where

these externalities act do not allocate resources efficiently, since prices do not reflect this

phenomenon, causing what is called a market failure. Within this framework, the public sector and the

authorities are justified in acting to solve the problem and achieve the economic-social efficiency of

these activities where the phenomenon is manifested

(Acquatella, 2001), trying to modify the behavior (rational, based on the information processed) of the agents that cause environmental degradation.

The protection of the environment is a challenge for humanity that entails a firm commitment

by society, governments and organizations to carry out actions for its protection, which underlies

the need for environmental management within all organizations.

Hence, the importance of government management, supported by science and innovation,

aimed at addressing the major challenges facing the country, which seeks to strengthen

decision-making at all levels and in all areas with the support of expert knowledge, while allowing experts to

find more expeditious ways to advance their proposals (Díaz-Canel Bermúdez et al., 2020).

There are many definitions of the concept of economic instruments. Most of these

definitions follow the Organization for Economic Cooperation and Development

(2020), which indicates that economic instruments are mechanisms that influence the costs and benefits of the

different options offered to economic agents and seek to modify behaviors in an environmentally

friendly way.

Financial economic instruments aim to close the gap between private and social costs

by internalizing all external costs (both depletion and pollution costs) to their sources: the

producers and consumers of the commodities that deplete and pollute the resources (Panayotou, 1995).

An economic financial instrument is any tool or method used by an organization to

achieve general development objectives in the production or regulation of material resources.

Economic financial instruments are fiscal and economic incentives and disincentives to

incorporate environmental costs and benefits into household and business budgets. The aim is to

encourage environmentally sound and efficient production and consumption through full-cost pricing.

Economic instruments include effluent taxes or charges on pollutants and wastes, deposit-refund

systems, and tradable pollution permits. In all cases, they aim to value ecosystem services and seek

the internalization of environmental externalities by the potential polluter or user of an

environmental resource (Morrissey, 2020).

According to the authors, economic instruments are incentives designed by all levels of

government within the scope of their competences, with the purpose that legal or natural persons

show changes in their behavior and assume the costs related to the actions they carry out as

a consequence of the ecosystem goods and services from which they benefit, directly or

indirectly for their productions or services.

An economic instrument for managing the environment is a policy or combination of policies

that provides financial economic incentives for users of natural resources to pay the social costs

of that use (Vraèareviæ, 2014).

Economic instruments, including taxes on effluents or charges on pollutants and wastes,

are tools for improving management efficiency and can be linked to the development of

environmental policies under cost-benefit and cost-efficiency criteria, with the development, at the same

time, of self-financing capacity.

They are defined as financial and fiscal measures that help to encourage, motivate or

incentivize the behavior of individuals to reduce pollution and degradation of natural resources. Two

important functions are assigned to these instruments: the incentive to reduce pollution and to

promote research and development of clean technologies

(Barragán Muñoz & de Andrés García,

2020).

They regulate social interventions in the market economy.

It is the result of the combination of financial means, technical knowledge and human skills.

Financial or market economic instruments are considered to be those through which

people assume the benefits and costs related to climate change mitigation and adaptation,

encouraging them to carry out actions that favor compliance with the objectives of the national policy on

the subject.

The design of these financial economic instruments is based on the principles of

environmental law of whom pollutes, pays prevention, precaution, participation and access to information,

to mention the most important ones, constitutes the basis for their design and are considered

from a legal and economic point of view, since they imply the polluting agent to assume the costs

of prevention and environmental remediation, with differentiated responsibilities.

These are certain financial and fiscal measures that help to encourage, motivate or

incentivize the behavior of individuals to reduce pollution and degradation of natural resources.

These instruments are assigned two important functions: that of an incentive to reduce pollution

and that of promoting research and development of clean technologies. They have been

organized into three types: a) those that have been translated into fiscal policy tools and generally

punish polluters; b) subsidies coupled to production; and, c) payments to reward environmentally

desirable behavior.

Economic and financial instruments can be used to change people's behavior towards

desired policy objectives, typically encompass a wide range of designs and implementation

approaches, and include traditional fiscal instruments, including, for example, subsidies, taxes, fees and

fiscal transfers. In addition, instruments such as tradable pollution permits or tradable land

development rights depend on the creation of new markets. Other instruments represent conditional

and voluntary incentive schemes such as payments for ecosystem services.

In principle, all of these can be used to correct policy or market failures and restore

full-cost pricing. They aim to reflect the social costs or benefits of the conservation and use of

biodiversity and ecosystem services of a public good nature. Economic instruments do not necessarily

imply that they promote the merchandizing of environmental functions. In general, they are

intended to change the behavior of individuals (e.g., consumers and producers) and public actors

(e.g., local and regional governments).

Economic financial instruments influence environmental performance by changing the cost

and benefits of alternative actions available to economic agents (OECD, 2020).

Economic and financial instruments aim to provide signals and incentives to stimulate

behavioral change throughout the value chain and generate benefits (Adelegan & Itesi, 2019), using

integrated economic valuation of ecosystem goods and services as a tool for decision making at

different levels, related to legal, policy and institutional frameworks in key sectors, optimizing the

generation of global environmental benefits

Economic instruments are tools for improving management effectiveness and can be subject

to the development of environmental policies under cost-benefit and cost-efficiency criteria,

with the development, at the same time, of self-financing capacity (Vidal Hernández et al., 2021).

These mainly seek to change the behavior of regulated agents to achieve environmental

objectives (pollution abatement, efficient use of natural resources, among others), through market

signals or taxes, for example, economic incentives, tax benefits, fees and taxes, among others,

these are aimed at recognizing actions that generate positive effects for society (increase

positive externalities) and avoid and control the unfavorable impacts of certain actions (decrease

negative externalities), in addition to directing, collecting and executing resources to finance the

policy, programs or plans or to cover the risks of the activities with positive impact that are expected

to be promoted. This group includes the financial products and services of the main private

and public financial entities, credit lines and financing funds

(Biointropic, 2022).

Economic instruments are essential mechanisms for financing conservation, since

many environmental services and costs are external to the finances of private companies.

Economic instruments are efficient means for governments to bring these externalities to market

prices (Cepal, 2022).

Economic financial instruments are a tool that primarily seeks to incentivize,

compensate, benefit, support or induce a change in the agents involved by charging or assigning

an economic value represented in a fee, price or cost. They have been applied primarily

to respond to specific situations, generally driven by a mix of ecological and

economic considerations (Monzón Aldama et al.,

2022). They use market forces to integrate

economic and environmental decisions. They should provide tariffs, prices or costs to help

decision makers recognize the environmental implications of their actions with the aim of

minimizing ecological damage.

Table 1. Concepts of economic and financial instruments for environmental management

Author |

Year |

Concept |

Panayotou |

1995 |

Financial economic instruments aim to close the gap between private and social costs by internalizing all external costs (both depletion and pollution costs) to their sources: the producers and consumers of the commodities that deplete and pollute resources. |

Vračarević |

2014 |

An economic-financial instrument for managing the environment is a policy or combination of policies that provides economic-financial incentives for users of natural resources to pay the social costs of that use. |

Adelegan and Itesi |

2019 |

Economic and financial instruments aim to provide signals and incentives to stimulate behavioral change throughout the value chain and generate benefits. |

Barragán Muñoz and de Andrés García |

2020 |

Economic instruments are certain financial and fiscal measures that help to encourage, motivate or incentivize the behavior of individuals to reduce pollution and degradation of natural resources. These instruments are assigned two important functions: to provide incentives to reduce pollution and to encourage research and development of clean technologies. |

OECD |

2020 |

Economic and financial instruments influence environmental performance by modifying the cost and benefits of alternative actions available to economic agents. |

Vidal Hernández et al. |

2021 |

Economic instruments are tools for improving management effectiveness and can be subject to the development of environmental policies under cost-benefit and cost-efficiency criteria, with the development, at the same time, of self-financing capacity. |

Biointropic |

2022 |

They mainly seek to change the behavior of regulated agents to achieve environmental objectives through market signals or taxes aimed at recognizing actions that generate positive effects for society and to avoid and control the unfavorable impacts of certain actions. |

Monzón Aldama et al. |

2022 |

Economic instruments are a tool that primarily seeks to incentivize, compensate, benefit, support or induce a change in the agents involved by charging or assigning an economic value in the form of a fee, price or cost. They have been applied primarily to respond to specific situations, generally driven by a mix of ecological and economic considerations. |

Source: Own elaboration based on the works previously mentioned

Based on the information compiled in the table above, the concept of economic and

financial instruments for environmental management can be defined, unifying the criteria of the

different authors, as described below:

Economic and financial instruments are a combination of policies composed of tools,

methods and actions that primarily seek to incentivize, compensate, benefit, support or induce a change

in the agents involved by charging or assigning an economic value represented in a fee, price

or cost. They are applied primarily to respond to specific situations, generally driven by a mix

of ecological and economic considerations to encourage environmentally sound and

efficient production and consumption.

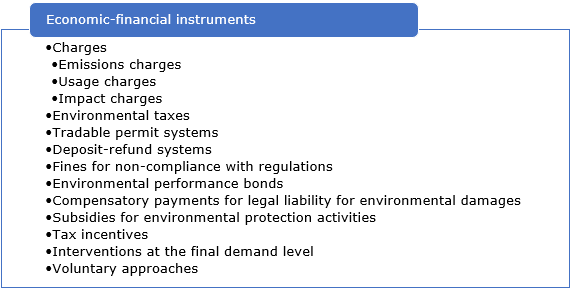

Classification of financial economic instruments applicable to environmental management

According to Monzón Aldama et al. (2022),

economic-financial instruments are classified into

the following categories (Figure 1):

Figure 1. Classifications of economic and financial instruments

Source: Own elaboration

For each type of instrument, Biointropic (2022) defines an internal classification according to

its nature and from the point of view of environmental management as presented in the

following table the classifications considered for each instrument typology.

Table 2. Classifications for each type of instrument

Typology |

Categories |

Definition |

Economic instruments |

Taxes (Contributions and discounts) |

These refer to different types of taxes or levies that are expected to generate a specific behavior of the agents so as not to cause them or if they are caused, and generate a positive impact, they are discounted or refunded.

There are environmental taxes that help finance environmental policy by charging for actions that have a negative impact on the environment, mainly seeking to change the behavior of the regulated agents.

There are also tax incentives understood as tax benefits for individuals or legal entities for behavior or investment with positive impacts on the environment or natural resource management. |

National income |

This corresponds to all the income received by a given population over the course of a fiscal year, and is converted into the national budget, with the possibility of earmarking it for specific items, in this case for processes to promote and consolidate green businesses. |

Market |

They are those created for economic agents to trade the positive or negative externalities generated by their activities through markets (Examples: conservation banks, environmental offsets, tradable permits, carbon market, among others), seeking to change behaviors and reach permitted levels of pollution, without the need to impose command and control mechanisms. |

Economic incentives |

They are those that encourage people to improve in certain aspects, motivating the sustainable production that comprises a green business. It can be considered as an economic benefit (in money or in kind) to be granted to people after fulfilling a certain action. Therefore, an incentive is something that motivates people to achieve environmental objectives. |

Financial instruments |

Credit |

It is a loan of money given to a natural or legal person with the commitment to repay the amount received, plus a percentage of interest to be paid within a certain period of time, which is defined between the creditor and the debtor. In this case, the creditor is the person or enterprise that lends the money and has the right to collect it. And the debtor is the individual or organization that owes the amount of money lent (plus interest) and is obliged to pay it. |

Environmental and productive trust funds |

They are vehicles for channeling aid funds from governmental (multi- or bilateral aid) and non-governmental donors, which are administered by a fiduciary organization. Trust funds are dedicated to financing activities agreed upon by the trustee organization and the donor(s). The activities to be financed can be linked to global programs or to specific projects, in this case those aimed at financing activities related to the promotion and consolidation of green businesses. |

Environmental impact investment funds |

They are a collective investment institution composed of a group of participants, where individuals or legal entities pool money to invest it in financial assets, in order to obtain an economic return, while maintaining the security and liquidity of their capital.

Therefore, investment funds with environmental impact can be understood as those that offer various types of returns on the investment of the available capital, one is the traditional financial return, another is the environmental return by contributing to improving the quality of life, for example, investment to reduce the emission of greenhouse gases and a reputational return by contributing to the fulfillment of public agendas and development objectives. |

Promotional tools |

Technical training programs |

They aim to prepare people in specific areas of the productive sectors of green business and develop specific technical competencies related to the consolidation of the business individually or collectively. |

Programs to promote production and marketing |

Their purpose is to encourage enterprises interested in the production and commercialization of goods and services associated with green businesses, through different spaces and promotional mechanisms, which seek to increase the attraction of investment and job creation. |

Recognition programs |

They are a strategy to promote the generation of goods and services with positive environmental, social and environmental impacts, based on the granting of recognitions, awards, certifications, etc., which represent a guarantee of the work carried out in order to obtain greater benefits with commercial partners. |

Source: Biointropic (2022)

The different classifications of economic and financial instruments that have been used

in environmental matters have, in general, proven to be a good complement to the

regulatory action of the State. Their good design makes it possible to adequately internalize

externalities, generate the appropriate incentives in the different actors of society and favor the efficient use

of resources.

Economic and financial instruments for environmental management regulated in Cuba

Effective environmental management achieves the protection of the environment and the

reduction of its increasingly evident deterioration. Economic instruments play an important role since

they focus on the economic interest of the actors and usually act before the undesired effect

takes place (Monzón Aldama et al., 2022).

Economic regulation as a management tool and even as an instrument to promote the

rational use of natural resources has made its presence felt in our country.

The legal and more general support for the use of economic instruments in Cuba is provided

by the Draft Law of the Natural Resources and Environment System (Law 150/2022), approved

by the National Assembly of People's Power in May 2022, which legally supports the policy

outlined by the National Environmental Strategy of the same year and develops the general legal

framework for its application.

This, according to Article 3, paragraph b, has among its specific objectives to establish the

principles and obligations that guide the actions of natural and legal persons in environmental

matters, including coordination mechanisms for efficient environmental management, as well as

(paragraph c) to establish the institutional framework for the protection of the environment and

ensure conservation, protection and rational use of natural resources and to perfect the

instruments (paragraph f) of environmental policy, control and management, in its conception and

expansion in development schemes, with emphasis on mechanisms of an economic and social nature,

aimed at the solution of environmental problems.

Article 10.1 states that Citma is responsible for: (paragraph j)

designing and promoting the implementation of economic instruments aimed at protecting the environment and natural

resources and recognizing the value of ecosystem goods and services.

Article 21.1 defines that Citma, without prejudice to the powers of the Ministry of Agriculture

with respect to wild flora and fauna and of the Ministry of Food Industry, in relation to the

production of hydrobiological resources, directs actions aimed at: (item r) adopting or proposing the

adoption, as appropriate, of economic and social incentives and instruments for the conservation and

rational use of biological diversity.

In turn, Article 22 states that natural and legal persons, in charge of the administration of

natural resources for the conservation, rational use and

access to biological diversity, have, as

appropriate, the responsibility to: (item h) implement economic instruments that stimulate the

conservation of biological diversity.

Article 72 establishes that it is incumbent upon Citma, in its role as the governing body of

the Environmental Resources and Environment System, to execute, as appropriate, the

promotion (subsection d) of the development of economic and financial instruments that discourage

the generation of waste and encourage best practices to reduce pollution and save

natural resources.

Article 106 explains that the present Law and its complementary provisions are

implemented through environmental management instruments of an economic nature (subsection k).

Similarly, Article 169 states that Citma, with respect to the processes of economic valuation

of ecosystem goods and services, coordinates the work for their gradual introduction in

the country, starting with:

Subsection b: Design or improve methodologies for the economic valuation of

environmental damages in the event of extreme events.

Subsection c: Incorporate the results of economic valuation studies in planning, the design

of public policies and in the decision-making process on projects, plans, policies in

strategic development sectors, as well as in the economic valuation of environmental damage

from extreme events.

Subsection d: to serve as a basis for the foundation of the economic and financial

mechanisms that so require.

This Law defines economic regulation as an instrument of environmental management

based on two principles: the principle of prevention and the principle commonly known as

"the polluter pays", which, unlike what is normally understood, is not mainly referred to

payment, to which a sanction refers the possible violator, but is basically a principle of cost allocation,

so that the environmental costs are borne by those responsible for the pollution and not

charged to society.

As a result, the prices of goods can be expected to reflect the real cost of production,

including that associated with pollution, resource degradation and environmental damage in

general (Monzón Aldama et al., 2022).

It is considered a law based on the ecosystemic approach to management, where its

main objective is to ensure the implementation and operation of the Natural Resources

and Environment System, as a condition to achieve the prosperous and sustainable development

of the country and, in turn, respond to the socialist development model advocated by each

and every Cuban and the call made by the country's leadership. Its institutional

framework strengthens Citma's role before the rest of the agencies and entities that manage

natural resources, while recognizing the competencies that they must assume in these matters.

The purpose of Law No. 113/2012 on the Tax System is to establish the taxes, principles,

rules and general procedures on which the Tax System of the Republic of Cuba is

based.

To solve the environmental problems facing the country, it is necessary to use all

available tools. The mission of solving the complex problems of

deforestation, soil erosion, overexploitation of aquifers, and water and air pollution will require changes in the behavior

of households, enterprises and governments, because the economic decisions of these

three agents are the most important force in the transformation and use of natural resources. It

will also require the definition of economic and financial instruments for their

subsequent application and appropriate use.

It is important that they be pushed forward decisively and that polluters face the costs of

their decisions: increasing the cost of using dirty fuels, increasing the cost of polluting water or

the cost of improperly disposing of waste.

Likewise, conservation and environmental care activities should be rewarded

through preferential credits; subsidies should be granted to sustainable activities (with the objective

of promoting them) through economic aid, such as organic agriculture and recycling

plants, among others.

Economic agents (consumers, businessmen, government, etc.) need to change their

behavior and incorporate the social costs of their actions. Just as the employer and the worker have

a remuneration, nature must have its own, and this must be adequate to replenish the

almost three centuries of intensive exploitation.

REFERENCES

Acquatella, J. (2001). Aplicación de instrumentos económicos en la gestión ambiental en

América Latina y el Caribe: Desafíos y factores

condicionantes. Comisión Económica para

América Latina y el Caribe. https://repositorio.cepal.org/handle/11362/5715

Adelegan, A. E., & Itesi, N. S. (2019). Economic Instruments for Environmental Sustainability

in the Nigerian Oil and Gas Sector. Saudi Journal of Economics and

Finance, 3(12), 610-619. https://doi.org/10.36348/sjef.2019.v03i12.005

Barragán Muñoz, J. M., & de Andrés García, M. (2020). La gestión de los sistemas

socio-ecológicos de la Bahía de Cádiz: ¿nuevas políticas públicas con viejos instrumentos? Boletín de la Asociación de Geógrafos

Españoles, (85), 1-42. https://doi.org/10.21138/bage.2866

Biointropic. (2022). Consultoría para la actualización del Plan Nacional de Negocios

Verdes (Mecanismos e incentivos tributarios y no tributarios; instrumentos financieros,

económicos, monetarios y no monetarios). Inter-American Development Bank (HQ).

https://www.minambiente.gov.co/wp-content/uploads/2022/05/E3-Instrumentos-econoimicos-financieros-y-de-promocioin-NV-11-05-2022.pdf

Canova, M. A., Lapola, D. M., Pinho, P., Dick, J., Patricio, G. B., & Priess, J. A. (2019).

Different ecosystem services, same (dis)satisfaction with compensation: A critical

comparison between farmers' perception in Scotland and Brazil. Ecosystem Services, 35, 164-172. https://doi.org/10.1016/j.ecoser.2018.10.005

Cepal. (2022). Estudio Económico de América Latina y el Caribe 2022: Dinámica y desafíos de

la inversión para impulsar una recuperación sostenible e

inclusiva (LC/PUB.2022/9-P/Rev.1). Comisión Económica para América Latina y el Caribe.

https://www.cepal.org/es/publicaciones/48077-estudio-economico-america-latina-caribe-2022-dinamica-desafios-la-inversion

Damania, R., Sterner, T., & Whittington, D. (2020). Environmental policy instruments and

corruption. China Economic Journal,

13(2), 123-138. https://doi.org/10.1080/17538963.2020.1751454

Díaz-Canel Bermúdez, M., Núñez Jover, J., & Torres Paez, C. C. (2020). Ciencia e innovación

como pilar de la gestión de gobierno: Un camino hacia los sistemas alimentarios

locales. Cooperativismo y Desarrollo,

8(3), 367-387.

https://coodes.upr.edu.cu/index.php/coodes/article/view/372

Durango, S., Sierra, L., Quintero, M., Sachet, E., Paz, P., Silva, M. A. da, Valencia, J., & Le Coq,

J.-F. (2019). Estado y perspectivas de los recursos naturales y los ecosistemas en

América Latina y el Caribe (ALC). Food and Agriculture Organization of the United Nations -

FAO. https://cgspace.cgiar.org/handle/10568/102446

Koellner, T., Bonn, A., Arnhold, S., Bagstad, K. J., Fridman, D., Guerra, C. A., Kastner, T.,

Kissinger, M., Kleemann, J., Kuhlicke, C., Liu, J., López-Hoffman, L., Marques, A., Martín-López,

B., Schulp, C. J. E., Wolff, S., & Schröter, M. (2019). Guidance for assessing

interregional ecosystem service flows. Ecological

Indicators, 105, 92-106.

https://doi.org/10.1016/j.ecolind.2019.04.046

Molina, J. R., & Rodríguez y Silva, F. (2019). Valuation of the economic impact of wildland fires

on landscape and recreation resources: A proposal to incorporate them on damages

valuation. En Proceedings of the fifth international symposium on fire economics, planning, and

policy: Ecosystem services and wildfires (pp. 228-238). Department of Agriculture, Forest

Service, Pacific Southwest Research Station. https://www.fs.usda.gov/research/treesearch/57688

Monzón Aldama, Y., Pérez Díaz, S., Marrero Marrero, M., & Petersson Roldán, M.

(2022). Aproximación teórica de instrumentos y mecanismos económico-financieros para la

gestión ambiental de bahías. Cooperativismo y

Desarrollo, 10(1), 161-186. https://coodes.upr.edu.cu/index.php/coodes/article/view/490

Morrissey, K. (2020). Resource and Environmental Economics. En

International Encyclopedia of Human

Geography (2.a ed., pp. 463-466). Elsevier.

https://doi.org/10.1016/B978-0-08-102295-5.10755-3

OECD. (2020). Policy instruments and finance for developing countries to promote the

conservation and sustainable use of the ocean. En

Sustainable Ocean for All: Harnessing the Benefits

of Sustainable Ocean Economies for Developing

Countries (pp. 73-110). Organización

para la Cooperación y el Desarrollo Económicos.

https://www.oecd-ilibrary.org/development/sustainable-ocean-for-all_bede6513-en

Panayotou, T. (1995). Economic Instruments for Environmental Management and

Sustainable Development. United Nations Environment Programme.

https://wedocs.unep.org/xmlui/handle/20.500.11822/28543

Pérez Calderón, J. (2010). La política ambiental en México: Gestión e instrumentos

económicos. El Cotidiano, (162), 91-97. https://www.redalyc.org/articulo.oa?id=32513882011

Vargas, L., Willemen, L., & Hein, L. (2019). Assessing the Capacity of Ecosystems to

Supply Ecosystem Services Using Remote Sensing and An Ecosystem Accounting

Approach. Environmental Management,

63(1), 1-15. https://doi.org/10.1007/s00267-018-1110-x

Vázquez Sosa, A., Frausto Martínez, O., & Cabrera Hernández, J. A. (2020). Modelos del

Manejo Integrado de Zonas Costeras: Análisis Comparativo y Propuesta de Adopción para el

Caso de Akumal (México). Costas,

2(1). https://revistas.uca.es/index.php/costas/article/view/8938

Vidal Hernández, L., de Yta Castillo, D., Castellanos Basto, B., Suárez Castro, M., & Rivera

Arriaga, E. (2021). Fiscal Economic Instruments for the Sustainable Management of

Natural Resources in Coastal Marine Areas of the Yucatan Peninsula. Sustainability, 13(19), 11103. https://doi.org/10.3390/su131911103

Vihervaara, P., Viinikka, A., Brander, L., Santos Martín, F., Poikolainen, L., & Nedkov, S.

(2019). Methodological interlinkages for mapping ecosystem services - from data to analysis

and decision-support. One Ecosystem,

4, e26368. https://doi.org/10.3897/oneeco.4.e26368

Vraèareviæ, B. (2014). Economic instruments in environmental policy. The Environment, 2.

https://www.researchgate.net/publication/324165196_Economic_instruments_in_environmental_policy

Conflict of interest

Authors declare that they have no conflicts of interest.

Authors' contribution

Yenisleidys Monzón Aldama and Sheila Pérez Díaz designed the study, analyzed the data and prepared the draft.

María Leandra Pascua Migueles was involved in data collection.

Mercedes Marrero Marrero and Maritza Petersson Roldán were involved in data collection, analysis and interpretation.

All the authors reviewed the writing of the manuscript and approve the version finally submitted.

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License