https://orcid.org/0000-0001-8141-283X

https://orcid.org/0000-0001-8141-283X mcruz@upr.edu.cu

mcruz@upr.edu.cu

Cooperativismo y Desarrollo, September-December 2021; 9(3), 957-985

Translated from the original in Spanish

Methodology to implement corporate social responsibility indicators that impact local development

Metodología para implementar indicadores de responsabilidad social empresarial que impacten en el desarrollo local

Metodologia para implementar indicadores de responsabilidade social corporativa, de impacto para o desenvolvimento local

Martha María Cruz Bravo1; Noraida Garbizo Flores2; Alba Marina Lezcano Gil3

1 Universidad de Pinar del Río "Hermanos Saíz Montes de Oca". Centro Universitario Municipal

de Consolación del Sur. Pinar del Río, Cuba.

https://orcid.org/0000-0001-8141-283X

mcruz@upr.edu.cu

2 Universidad de Pinar del Río "Hermanos Saíz Montes de Oca". Centro Universitario Municipal

de Consolación del Sur. Pinar del Río, Cuba.

https://orcid.org/0000-0003-3109-468X

norita@upr.edu.cu

3 Universidad de Pinar del Río "Hermanos Saíz Montes de Oca". Centro Universitario Municipal

de Consolación del Sur. Pinar del Río, Cuba.

https://orcid.org/0000-0001-8574-8859

marina@upr.edu.cu

Received: 25/07/2021

Accepted: 19/12/2021

ABSTRACT

The proposals for models and other ways of measuring Corporate Social Responsibility have been diverse in recent decades, ranging from the analysis of sustainability reports provided by enterprises to the application of single and multiple indicators. Of the latter, very few are those formulated to measure the impact on the territory of enterprise activities that are developed from the use of indicators contextualized to local environments, for which it is important to have guides that methodologically allow to evaluate, in an accurate way, the socially responsible performance of enterprises in the territories. The objective of this work is: to design a methodology for the implementation of a System of Municipal Corporate Social Responsibility Indicators, which allows the municipal government to evaluate the socially responsible management and the social commitment of the local enterprise community, with a focus on interest groups and forging a culture of production and services that enhances sustainable local development and community welfare, validating it through the use of the Delphi method, as a method of consultation with experts.

Keywords: local development; dimensions; stakeholders; methodology; corporate social responsibility

RESUMEN

Las propuestas de modelos y otras formas de medir la Responsabilidad Social Empresarial han sido diversas en las últimas décadas; estas van desde el análisis de informes de sostenibilidad, que proporcionan las empresas, hasta la aplicación de indicadores únicos y múltiples. De estos últimos, muy pocas son las formuladas para medir el impacto en el territorio de las actividades empresariales que se desarrollan a partir de la utilización de indicadores contextualizados a los entornos locales, para lo cual es importante contar con guías que metodológicamente permitan evaluar, de manera acertada, la actuación socialmente responsable de las empresas en los territorios. El objetivo de este trabajo es: diseñar una metodología para la implementación de un Sistema de indicadores de Responsabilidad Social Empresarial Municipal, que permita al gobierno municipal evaluar la gestión socialmente responsable y el compromiso social del empresariado local, con enfoque de grupos de interés e ir forjando una cultura de producción y servicios que potencie el desarrollo local sostenible y el bienestar comunitario, validando la misma a través del uso del método Delphi, como método de consulta a expertos.

Palabras clave: desarrollo local; dimensiones; grupos de interés; metodología; responsabilidad social empresarial

RESUMO

As propostas de modelos e outras formas de medir a Responsabilidade Social Corporativa têm sido diversas nas últimas décadas, desde a análise dos relatórios de sustentabilidade fornecidos pelas empresas até a aplicação de indicadores únicos e múltiplos. Destes últimos, muito poucos são formulados para medir o impacto no território das atividades empresariais que são desenvolvidas a partir do uso de indicadores contextualizados aos ambientes locais, para os quais é importante ter guias que permitam metodologicamente avaliar, de forma precisa, o desempenho socialmente responsável das empresas nos territórios. O objetivo deste trabalho é: elaborar uma metodologia para a implementação de um Sistema de Indicadores de Responsabilidade Social Empresarial Municipal, que permita ao governo municipal avaliar a gestão socialmente responsável e o compromisso social das empresas locais, com foco nas partes interessadas e forjar uma cultura de produção e serviços que aumente o desenvolvimento local sustentável e o bem-estar da comunidade, validando-o através do uso do método Delphi, como método de consulta a especialistas.

Palavras-chave: desenvolvimento local; dimensões; partes interessadas; metodologia; responsabilidade social corporativa

INTRODUCTION

Enterprises create and develop their processes in a local environment, so in carrying out their activities they cannot be oblivious to the environment in which they operate, as it is impossible for them to operate without affecting or being affected by that environment. Hence the need for the management models to be used to respect the needs, expectations, concerns and interests of the different interest groups, above all, of the locality in which it is located, which presupposes the awareness of entrepreneurs and local governments that the legitimacy to operate and carry out the activities inherent to them is granted by the interest groups with which they relate and that these models must have as their main basis, sustainability from the social, economic and environmental point of view.

It is recurrent nowadays that the decisions of economic and social development policies in key actors are marked by the stakeholder approach, it is increasingly widespread; therefore, the vast majority of recent research proposals on Corporate Social Responsibility (CSR), focus on the creation of value by the enterprise towards its main stakeholders (Díaz de la Cruz & Fernández Fernández, 2016).

The World Council for Sustainable Development defines Corporate Social Responsibility as the "continuous commitment by enterprises to behave ethically and contribute to sustainable economic development, while improving the quality of life of workers and their families, as well as the local community and society in general", a concept collected in the work done by Díaz de la Cruz and Fernández Fernández (2016) becomes a kind of axis so that the State, based on this idea, can promote responsible practices in the enterprise sector with all of its stakeholders. (Saltos Orrala & Velázquez Ávila, 2019).

What it is about, then, is to forge a culture that contributes to integrate to the management models, good enterprise practices that contribute to sustainable local development, incorporating real strategies around Corporate Social Responsibility, so that it becomes a transversal axis of the integrated system of enterprise management, identifying entrepreneurs and local governments with a more responsible public image. "(...) Social Responsibility is a theory of management that obliges the organization to place itself and commit itself socially in and from the very exercise of its basic functions. Of course, it is the same organizational management that is socially responsible and not one of its marginal appendices (...)" (Vallaeys, 2007).

Since the 20s of the last century until today, there have been multiple definitions established by different authors, associated with Social Responsibility and Corporate Social Responsibility, among which the following stand out; international standards have also been designed that address the issue from different perspectives and dimensions: social, environmental, economic and ethical. Corporate Social Responsibility, in complex terms, is defined as the combination of voluntary actions by enterprises, with the aim of providing solutions to social and environmental problems, incorporating them into their commercial procedures policies and, in particular, in their relations with their stakeholders (Morell Jiménez, 2019).

In the last decades, a quite discussed aspect is the problem of CSR measurement. It was possible to determine that the main proposals for this type of measurement are related to (1) the analysis of the reports submitted by the enterprises and (2) the formulation of single and multiple indicators (Puentes López & Lis Gutiérrez, 2018). Despite the efforts made, there is still no consensus on the solution to this problem due to the objective and subjective difficulties encountered in its measurement and the great diversity of indicators that does not allow an effective application of the same in the recognized dimensions of CSR: social, environmental, ethical and especially economic, specifically, the latter dimension has been the most controversial in terms of its relevance and the most effective way to measure it from the perspective of CSR.

According to Puentes and Lis-Gutiérrez (2018), the review of ways to measure CSR allowed grouping them mainly into two types: CSR reports and single and multiple indicators. This classification includes a wide range of proposals and combinations of indicators; most have been based on the sustainability reports of the Global Reporting Initiative, an independent institution that functions as an official collaboration center of the United Nations Environment Program, in which representatives of human rights organizations, labor rights, research centers, environmental organizations, corporations, investors and accounting organizations actively participate and which mission is to develop and disseminate the Guide for the Preparation of Sustainability Reports, which is instituted as an optional accounting report on sustainability. The Global Reporting Initiative, however, considered the first standard of its kind in the world, has not achieved its generalization as an instrument for measuring CSR.

In Latin America, a series of indicators have been disseminated in terms of measuring CSR, the Indicators of the Ethos Institute of Brazil (2012), which offer the possibility of measuring the commitment and socially responsible performance of enterprises and organizations of different types. The Ethos Institute is another of the organizations that, since 2000, has maintained a training program for media professionals in relation to CSR, with several editions on this topic. All this contributes to deepening the knowledge and dissemination of the subject and calls for reflection by the different social actors on the importance of enterprises reviewing their management practices.

The Ethos Indicators of Corporate Social Responsibility constitute, as a whole, a tool for the evaluation and planning of social responsibility processes in organizations. According to this organization, these indicators can be of different types: depth indicators (those that make it possible to evaluate the stage of an enterprise's CSR management), binary indicators and quantitative indicators.

Taken together, this structure of indicators allows the enterprise to plan how to strengthen its commitment to social responsibility. For example, it allows the enterprise to know what stage the organization is at and to establish the actions that need to be taken to move on to the next stage.

It is also important to objectively determine which CSR policies, socially responsible practices, models, etc., can be assumed by each organization, small, medium or large enterprise, taking into account the important relationship that exists between the resources of all kinds they have, the access to them, as well as the organizational capacities to assume complex political and strategic processes, as is the case of CSR, among other elements. However, there is consensus that the use of socially responsible management models in any size enterprise brings multiple benefits, both for the organization and for all its stakeholders, especially local communities.

Currently, there is a large number of private or public organizations and most of them want to obtain a distinctive or certificate that reflects the existence of socially responsible attitudes or practices within their enterprise activities, due to the benefits they bring, such as improving corporate image, attracting new consumers, increasing consumer loyalty indexes, among others (Herrera Acosta et al., 2020).

In general, organizations that have adopted CSR practices, to a greater or lesser extent, have established a working algorithm that allows, specifically for the enterprise sector, to follow certain guidelines that make the process of implementing CSR indicators feasible, especially methodologically, as it is one of the sectors that has the greatest impact on the sustainable socioeconomic development of any country. There are also a wide variety of practical guides and other ways to quantify the relationships established between CSR as a management philosophy and other aspects that are key to the development and growth of business organizations.

In the quantification of CSR and other organizational aspects, such as: financial performance, quality, reputation, there is no consensus in the results obtained by different researchers; but studies show positive correlation between social responsibility and the various related variables (... ), this being an aspect in favor of this form of enterprise management that gives it greater relevance and validity in the management field (Bermudez Colina & Mejías Acosta, 2018).

Currently, it is considered key in the socially responsible management of the enterprise sector to establish guidelines for measuring the level of integration of social management policies to the development strategies of each organization and the promotion of an organizational culture that promotes greater commitment to the objectives and mission of the organization and the local development strategy.

The establishment of the organization's strategic guidelines by the corporate governance, as well as their subsequent communication and acceptance by its members, should favor decision-making at the individual and organizational level, which is in accordance with the ethical culture and CSR policies of the enterprise (Díaz de la Cruz & Fernández Fernández, 2016).

As important as the institution and application of a CSR policy, is to carry out a process of measuring the results obtained by the implementation of such CSR policies (Pérez Espinoza et al., 2016).

This presupposes the use of qualitative and quantitative indicators that allow, in this particular case, local governments to know how their organizations behave today with respect to CSR and how these are integrated into management models to achieve better enterprise performance, with an impact on local welfare in terms of meeting the objectives of sustainable local development.

In the specific case of Cuba, Social Responsibility is inherent to the existing socio-political system, which is essentially humanistic and participatory, however, at the level of enterprise and base structures of all kinds, it is not always considered a priority issue to achieve good performance and, therefore, they do not orient their management models from a socially responsible approach, so they are not very active in the areas of CSR. Corporate Social Responsibility is implicit and naturalized, but is exercised without enterprise autonomy in response to higher orientations (Betancourt Abio & Gómez Arencibia, 2021).

In the opinion of the authors, in Cuba, it would be important to develop models of indicators that take into account the characteristics and importance of the territory, that is, of the locality where they impact, both positively and negatively the enterprises and other organizations, in short, indicators that can be contextualized in a local environment, where the government assumes the leading role in their implementation, ensuring that enterprise activities are carried out on the basis of commitment and social responsibility for inclusive and multi-stakeholder local development, which enhances other variables such as innovation, ethical performance, the value chain approach, the development of strategic sectors, etc.

The updating of the Cuban Economic Model, the implementation of the Country's economic and social policy guidelines and the objectives of the 2030 Agenda for Sustainable Development, are important reasons for immediate progress in the process of gradually adopting good practices in CSR, leading to a real sustainable local development.

The inter-institutional work in an integrated manner of the main local actors, where the Municipal University Centre stands as the most important center in the management of knowledge and innovation, has made possible to identify certain weaknesses that hinder local development and, of course, the development of the country. Among these issues, there are some problems that are associated with the non-use of socially responsible management approaches, which are oriented towards a greater contribution to local development.

The above reasons support the realization of this work that aims to: design a methodology for the implementation of a System of Indicators of Corporate Social Responsibility at the Municipal level (Sirsem in Spanish), which allows the municipal government to evaluate the socially responsible management and social commitment of local enterprise community, with a focus on stakeholders and go forging a culture of production and services that enhances sustainable local development and community welfare, validating it through the use of the Delphi method, as a method of consultation with experts.

MATERIALS AND METHODS

The design of the methodology was based on a diagnosis carried out through two open group interviews; one with the members of the Local Development Group and the other with a group integrated by key local actors from the most important enterprises and organizations in the municipality, in terms of contributions to local development, oriented from innovation and sustainability.

The diagnosis aimed to determine the regularities on the state of the application of some socioeconomic and environmental indicators that can contribute to measure CSR in enterprises and enterprise and service organizations in the territory in the following areas: prevailing organizational system, enterprise ethics and values, quality of life of workers in the enterprise, commitment to the community, contribution to local development, care and preservation of the environment and the enterprise's relationship with stakeholders.

In order to corroborate the validity and effectiveness of the methodology to implement a Sirsem, which allows the government of the municipality of Consolación del Sur to have a tool that facilitates the process of evaluating the socially responsible behavior of enterprises in the territory in the social, economic, environmental and organizational system dimensions and prevailing values, it was decided to consult experts, using the Delphi method.

The use of this method was preceded by the realization of an important preliminary phase in which the expert selection procedure is applied, consisting in the self-assessment of the experts through a questionnaire, of their competences and the sources that allow them to argue their criteria on the topic in question in order to be able, subsequently, to determine the level of competence of each expert, previously selected on issues of local development, CSR and indicators that allow local governments to evaluate the socially responsible conduct of enterprise and other organizations in local environments.

RESULTS AND DISCUSSION

Among the main regularities of the diagnosis, the following were identified:

Multiple indicators are one of the most widely used approaches to measuring CSR, especially through systems of indicators that include various dimensions (social, governance, enterprise ethics, economic and environmental), which have become a way of measuring CSR actions and their results. However, in the framework of a territory, of a locality, it is necessary, as expressed, to contextualize these indicators and, in addition, to offer local governments methodological guidelines that allow, step by step, to properly and effectively implement a system of CSR indicators, enhancing enterprise performance, competitive success and inclusive sustainable local development, based on the Municipal Strategy for Local Development.

The theoretical, methodological and normative bases that supported the methodology were the following:

The proposed methodology consists of six stages, which are summarized below:

Stage I: Formation and training of the Group or team of experts in Corporate Social Responsibility for local development.

Objective: To form a team that is accountable to the top management of the government to develop and evaluate a management model, with a socially responsible approach in the locality.

Phase I: Design and selection of the group or team of CSR experts.

Main actions:

Phase II: Training of the group or team of CSR experts.

In this phase, the actions that distinguish it are:

Stage II: Diagnosis of the situation of enterprises in the territory in terms of Corporate Social Responsibility.

Objective: To determine how local organizations see themselves in their enterprise management, taking as a point of analysis the elements of CSR and whether they are oriented to meet their responsibility to local stakeholders.

Phase I: Compilation of the Social Responsibility actions currently carried out by enterprises in the territory.

Main actions:

Phase II: Design and application of the diagnostic instruments for members of local stakeholders and other organizations and institutions.

Main actions:

Stage III: Survey of current and future CSR actions of enterprises in the territory, linked to the Municipal Development Strategy.

Objective: To identify current and potential CSR actions in the enterprises under analysis, linked to the sustainable development objectives contained in the Municipal Development Strategy.

Main actions:

Stage IV: Design of the CSR indicators system for local development.

Objective: To build a system of indicators to facilitate, organize, evaluate and generalize the concept of CSR, from a local perspective with a socio-economic and environmental approach.

Phase I: Diagnosis of the status of the application of the main socio-economic and environmental indicators that contribute to measuring Corporate Social Responsibility.

Main actions:

Phase II: Design of the Corporate Social Responsibility Indicator System for local development.

Main actions:

In each dimension the following aspects should be taken into account: values, transparency and governance, internal public, environment, suppliers, consumers/customers, community, government and society.

Based on these topics, the indicators, their structure and content were defined. These are qualitative and quantitative and their level of applicability and enforceability depends on the size of the enterprise and/or the availability of information on the activity they carry out, which may mean that some indicators are not adjusted at the time of implementation. These indicators should move from one level to another as the business management model becomes more oriented towards a socially responsible approach, which will require commitment, planning and investment to reach higher levels.

Stage V: Implementation, monitoring and evaluation of the CSR Indicator System.

Objective: Establish qualitative and quantitative indicators that measure the ethical, economic, social and environmental performance of the enterprise with stakeholders, taking into account the results of the diagnosis, establishing actions for its evaluation and effectiveness.

Main actions:

Stage VI: Supervision and control

Objective: To evaluate the effectiveness of the Sirsem implementation process and its impact on the socially responsible conduct of the sectors of the economy in local development, preventively alerting on any shortcomings, deficiencies and current and potential risks in its implementation.

Main actions:

Results of the application of the Delphi method of consultation with experts

For the application of the Delphi method, 30 experts were selected for the study from the University of Pinar del Río (Center of Studies: CE-GESTA and Municipal University Center of Consolación del Sur), Félix Varela Center, Center of Psychological and Sociological Research of Havana and other professionals of production and government at the local level, who have researched and have important results in the topic in question. As shown in the following graph, 60% of the experts qualify in the topics of social responsibility and indicators for its evaluation and 40% in local development.

Graph 1 - Professional qualification of the experts selected to evaluate the methodology

Source: Elaborated by the authors

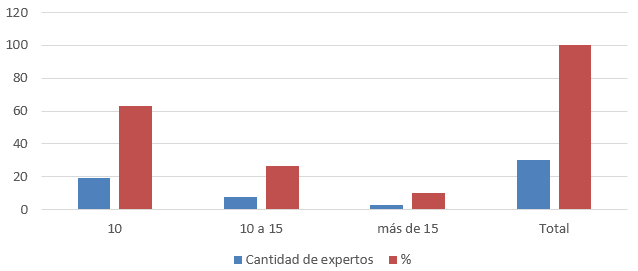

The years of experience of the selected experts in the topic under study are shown in the following graph:

Graph 2 - Years of experience of Social Responsibility and Local Development experts

Source: Elaborated by the authors

Of the selected experts, 20% are PhDs, 57% Masters of Science and 23% Specialists, which guarantees a good level of scientificity in the assessments to be made in the proposal under study.

As part of the preliminary phase and after selecting the experts to be consulted, those who met the requirements were subjected to a process of self-evaluation about the levels of information and argumentation they possessed on the topic in question.

For this purpose, a questionnaire was prepared in which, after being asked for certain general information about each of the experts, they were asked to mark with a cross, on an increasing scale from 1 to 10, the value that corresponds to the degree of knowledge or information they had about the topic of study.

From here, the coefficient of knowledge or information (Kc) could be calculated very easily. Subsequently, each expert carried out a self-assessment, according to the criteria set out in the following table to determine the coefficient of argumentation or substantiation (Ka) on the topic of study.

Table 1 - Factor pattern for determining the coefficient of argumentation (Ka)

Factor pattern |

High (A) |

Medium (M) |

Bass (B) |

1. Theoretical analyses carried out |

0.3 |

0.2 |

0.1 |

2. Experience gained |

0.5 |

0.4 |

0.2 |

3. Work by national authors |

0.05 |

0.05 |

0.05 |

4. Work by foreign authors |

0.05 |

0.05 |

0.05 |

5. Knowledge of the current state of the problem abroad |

0.05 |

0.05 |

0.05 |

6. Intuition |

0.05 |

0.05 |

0.05 |

TOTAL |

1 |

0.8 |

0.5 |

Source: Elaborated by the authors

Once the coefficients of knowledge (Kc) and argumentation (Ka), previously explained, were calculated, the coefficient of competence (K) of each expert was finally determined, through the equation: K = 0.5 (Kc + Ka).

From the self-assessment process of the experts, 63% of them obtained a high rating of their competence coefficient and the rest, 37%, obtained a medium rating of their competence coefficient, which shows a high level of competence to evaluate the proposal under assessment.

After the self-assessment process was concluded, the Delphi method was applied to validate the proposed methodology, which began with the delivery of a document to each expert that, in addition to other important aspects, contained the proposed methodology structured by stages and some of them organized by phases, with their respective actions, tools, methods and instruments to be used to meet the objectives proposed in each of them, in particular, and the overall goal of the methodology.

Next, a questionnaire was applied to evaluate the level of applicability and validity of the proposed methodology, taking into account 6 indicators detailed below. These indicators were:

In the exploratory phase of application of the Delphi method, two rounds were conducted with the same structure of the instrument to determine the results of the assessment of the methodology to implement the Sirsem by the selected experts.

Tables 2a, 2b, 2c and 2d show the results of the processing of the questionnaires and, as can be seen, the absolute frequencies vary between quite adequate and adequate to apply the methodology to implement the Sirsem. In the study presented, a high level of agreement between the opinions of the experts is evident. The results were reported to each expert in a timely manner.

Table 2a - Absolute frequencies

Indicators to assess |

C1-Sufficiently adequate |

C2-Very adequate |

C3-Adequate |

C4-Unsuitable |

C5-Not suitable |

TOTAL |

Ind 1 |

23 |

6 |

1 |

0 |

0 |

30 |

Ind 2 |

27 |

2 |

1 |

0 |

0 |

30 |

Ind 3 |

24 |

3 |

3 |

0 |

0 |

30 |

Ind 4 |

25 |

4 |

1 |

0 |

0 |

30 |

Ind 5 |

26 |

2 |

2 |

0 |

0 |

30 |

Ind 6 |

28 |

1 |

1 |

0 |

0 |

30 |

Source: Elaborated by the authors

Table 2b - Cumulative Frequency Matrix

Indicators to assess |

C1-Sufficiently adequate |

C2-Very adequate |

C3-Adequate |

C4-Unsuitable |

C5-Not suitable |

Ind 1 |

23 |

29 |

30 |

0 |

0 |

Ind 2 |

27 |

29 |

30 |

0 |

0 |

Ind 3 |

24 |

27 |

30 |

0 |

0 |

Ind 4 |

25 |

29 |

30 |

0 |

0 |

Ind 5 |

26 |

28 |

30 |

0 |

0 |

Ind 6 |

28 |

29 |

30 |

0 |

0 |

Source: Elaborated by the authors

Table 2c - Matrix of cumulative relative frequencies

Indicators to assess |

C1-Sufficiently adequate |

C2-Very adequate |

C3-Adequate |

Ind 1 |

0.766666667 |

0.966666667 |

1 |

Ind 2 |

0.9 |

0.966666667 |

1 |

Ind 3 |

0.8 |

0.9 |

1 |

Ind 4 |

0.833333333 |

0.966666667 |

1 |

Ind 5 |

0.866666667 |

0.933333333 |

1 |

Ind 6 |

0.933333333 |

0.966666667 |

1 |

Source: Elaborated by the authors

Table 2d - Image of the values of the relative cumulative frequencies by the inverse of the normal curve

Indicators for assessing the methodology |

C1-Sufficiently adequate |

C2-Very adequate |

Sum |

Average |

N-P |

I-1 |

0.73 |

1.83 |

2.56 |

1.281 |

-0.73 |

I-2 |

1.28 |

1.83 |

3.12 |

1.558 |

-1.01 |

I-3 |

0.84 |

1.28 |

2.12 |

1.062 |

-0.51 |

I-4 |

0.97 |

1.83 |

2.80 |

1.401 |

-0.85 |

I-5 |

1.11 |

1.50 |

2.61 |

1.306 |

-0.75 |

I-6 |

1.50 |

1.83 |

3.34 |

1.668 |

|

Sums |

6.43 |

10.12 |

16.55 |

8.27 |

-3.85 |

Limits or cut-off points |

1.29 |

2.02 |

1.65 |

||

N |

0.551622042 |

||||

Source: Elaborated by the authors

Next, the cumulative frequencies and relative frequencies are determined, as well as the cumulative relative frequencies and finally the values of the relative cumulative frequencies by the inverse of the normal curve to determine the cut-off points shown in tables 2a, 2b, 2c and 2d, which are used to establish the category or degree of adequacy of the methodology. In this case, the criteria issued by the experts were delimited in the categories: Fairly adequate (C1) and Very Adequate (C2).

The 100% of the experts approved the proposed stages; only a few opinions of a qualitative order and focus were expressed in the final part of the questionnaire, in which they could openly express their criteria. Based on the results of the second round, it was suggested by 3 of the experts to include in stage IV the design of a software with the same name as the system of indicators (Sirsem) and a self-assessment guide, in terms of CSR for enterprises and organizations in the municipality; this had an impact on the design of stage V: Implementation, monitoring and evaluation of Sirsem.

These criteria were studied to determine levels of agreement or divergences about the methodology, its structure and stages, which allowed complementing the same, phases, actions and instruments that make up the methodology, in order to achieve an effective implementation of the same.

After concluding the consultation with experts, through the Delphi method, it is concluded from the results obtained that the methodology to implement Sirsem and the software of the same name are viable for municipal environments to evaluate the social commitment of enterprises and other organizations with sustainable local development.

The previous results allowed the authors to design the final version of the methodology, as well as the content of each stage, which was approved by the Municipal Administration Body of the municipality of Consolación del Sur.

The final summarized version of the stages of the methodology, following the results of the expert consultation, is shown in the following graph:

Graph 3 - Stages of the methodology for implementing Sirsem

Source: Elaborated by the authors

From the results obtained in the validation of the methodology by the Delphi method, it was demonstrated the possibility of applying the methodology as a working tool of the government to implement a system of CSR indicators in the social, economic, environmental and organizational culture areas, which was complemented by the inclusion of several aspects suggested by the experts, especially in the stages of implementation of Sirsem and that of monitoring and control. This proposal, together with the system of indicators, will contribute to promote the formation of a local enterprise citizenship, with greater social responsibility, with sustainable, inclusive and multi-stakeholder local development.

REFERENCES

Bermudez Colina, Y., & Mejías Acosta, A. A. (2018). Medición de la responsabilidad social empresarial: Casos en pequeñas empresas latinoamericanas. Ingeniería Industrial, 39(3), 315-325. https://rii.cujae.edu.cu/index.php/revistaind/article/view/893

Betancourt Abio, R., & Gómez Arencibia, J. (2021). La Economía Social y Solidaria en Cuba: Fundamentos y prácticas para el desarrollo socialista. Publicaciones Acuario.

Díaz de la Cruz, C., & Fernández Fernández, J. L. (2016). Marco conceptual de la ética y la responsabilidad social empresarial: Un enfoque antropológico y estratégico. Revista Empresa y Humanismo, 19(2), 69-118. https://doi.org/10.15581/015.XIX.2.69-118

Herrera Acosta, J. F., Vásquez Torres, M. del C., & Ochoa Ávila, E. (2020). La evolución de la responsabilidad social empresarial a través de las teorías organizacionales. Revista Científica Visión de Futuro, 24(2), 80-104. https://revistacientifica.fce.unam.edu.ar/index.php/visiondefuturo/article/view/392

Instituto Ethos. (2012). Indicadores Ethos de responsabilidad social empresarial. Instituto Ethos de Empresas e Responsabilidade Socia. https://www.ethos.org.br/wp-content/uploads/2012/12/Indicadores-Ethos-Vers%C3%A3o-espanhol.pdf

Morell Jiménez, E. D. (2019). Responsabilidad Social Empresarial: Una radiografía sobre la situación de los grandes contribuyentes del sector comercial de la Ciudad de Pilar. Revista Internacional de Investigación en Ciencias Sociales, 15(2), 339-362. http://revistacientifica.uaa.edu.py/index.php/riics/article/view/835

Pérez Espinoza, M. J., Espinoza Carrión, C., & Peralta Mocha, B. (2016). La responsabilidad social empresarial y su enfoque ambiental:una visión sosteniblea futuro. Universidad y Sociedad, 8(3), 169-178. https://rus.ucf.edu.cu/index.php/rus/article/view/430

Puentes López, A., & Lis Gutiérrez, M. (2018). Medición de la responsabilidad social empresarial: Una revisión de la literatura. Suma de Negocios, 9(20), 145-152. https://doi.org/10.14349/sumneg/2018.V9.N20.A9

Saltos Orrala, M. A., & Velázquez Ávila, R. M. (2019). Apuntes teóricos para la promoción de la responsabilidad social empresarial en Ecuador. Revista ESPACIOS, 40(43). https://www.revistaespacios.com/a19v40n43/19404304.html

Vallaeys, F. (2007). Responsabilidad Social Universitaria: Propuesta para una definición madura y eficiente. Programa para la Formación en Humanidades - Tecnológico de Monterrey, México. http://bibliotecavirtualrs.com/2011/12/responsabilidad-social-universitaria-propuesta-para-una-definicion-madura-y-eficiente/

Conflict of interest:

Authors declare not to have any conflict of interest.

Authors' contribution:

Marta María Cruz Bravo and Noraida Garbizo Flores were in charge of designing the methodology for implementing a Corporate Social Responsibility Indicator System for local development, each of its stages and phases and the two preliminary revisions carried out until the final version was designed.

Alba Marina Lezcano Gil was in charge of the collection, analysis and interpretation of the information and the application of the Delphi method as a method for consulting experts to validate it.

All the authors reviewed the writing, coherence and unity between the objectives, development and conclusions, as well as the degree of contribution to the state of the art of the research carried out.

A thorough review was carried out by all the authors to approve the final version of the document submitted.